The New ICE Treasury Clearing Service – Explained

An outline of the new Intercontinental Exchange (ICE) Treasury Clearing Service (TCS) approach to trade novation, done-away and credit limits, trade and margin settlement, default resources and management, and margin segregation.

I am grateful to ICE for sharing documentation and spending time outlining and discussing their new clearing service.

Key takeaways

- ICE chose to build TCS in the ICE Clear Credit (ICC) legal entity, reusing components of their proven credit derivatives clearing service with modifications for US Treasuries (UST). This incorporates established features of derivatives trade flow, such as done-away trade clearing and pre-trade limit checking, which are new to the UST trade flow.

- TCS client margin is flexibly supported. Clients may agree to clear via a Net IM account (comingled with other entities) or a Gross IM account (mimicking the CFTC LSOC approach), and to split funding of gross IM with the clearing broker in three ways.

- Client margin is settled with ICC “indirect” (via the clearing broker), but client open trades are settled with ICC either indirect or direct.

- The default resources dedicated to TCS are structured similarly to those for ICC credit derivatives clearing. Note: in a participant default, ICC’s skin-in-the-game (SITG) capital is consumed before non-defaulting members’ guarantee funds.

- ICC is solely exposed to losses from a clearing participant Clearing brokers are solely exposed to losses from their client’s default.

Read on for more details of the TCS service or, if you have limited time, skip to the approach summary at the end.

Background

ICE recently announced that the U.S. Securities and Exchange Commission (SEC) has approved the ICC application and rulebook to expand its current Covered Clearing Agency (CCA) designation to add U.S. Treasury bond (UST) clearing.

TCS is now operationally live and ready to clear cash transactions. The clearing of repurchase agreements is expected before the June 2027 repo mandate go-live.

Much of the background for this blog concerning the SEC UST clearing mandate is covered in our posts from 2024. These include blogs on mandate scope, FICC’s clearing methods, CME’s UST clearing approach, FICC margin increases, bank financial impacts of UST clearing, buyside ways to reduce UST cleared margin, and guaranteed repo.

Everything below covers both cash UST trades and UST repo trades.

This blog does not discuss funding and capital impacts or compare the ICC TCS with any other UST clearing services.

Build approach, legal structure, and go-live timeline

ICE’s approach to building TCS has been to reuse features of their established credit derivatives clearing platform with adaptations, extensions, and additions to accommodate the UST-related differences in product, settlement channels, triparty agents, and the like.

TCS will be provided by the ICC legal entity, which currently houses ICE’s credit derivatives clearing service. Some elements of TCS must be separate and distinct from the ICC credit derivatives clearing service. Where existing organizational units or IT systems are reused, housing the service in ICC may help to reduce duplication and minimize effort and time-to-market. It will also open the path for standard features of OTC derivatives market infrastructure to be adopted in UST markets, where appropriate in the future.

With cash live and awaiting its first cleared trade, the go-lives for GC and DVP repo are expected before the mid-2027 mandate go-live.

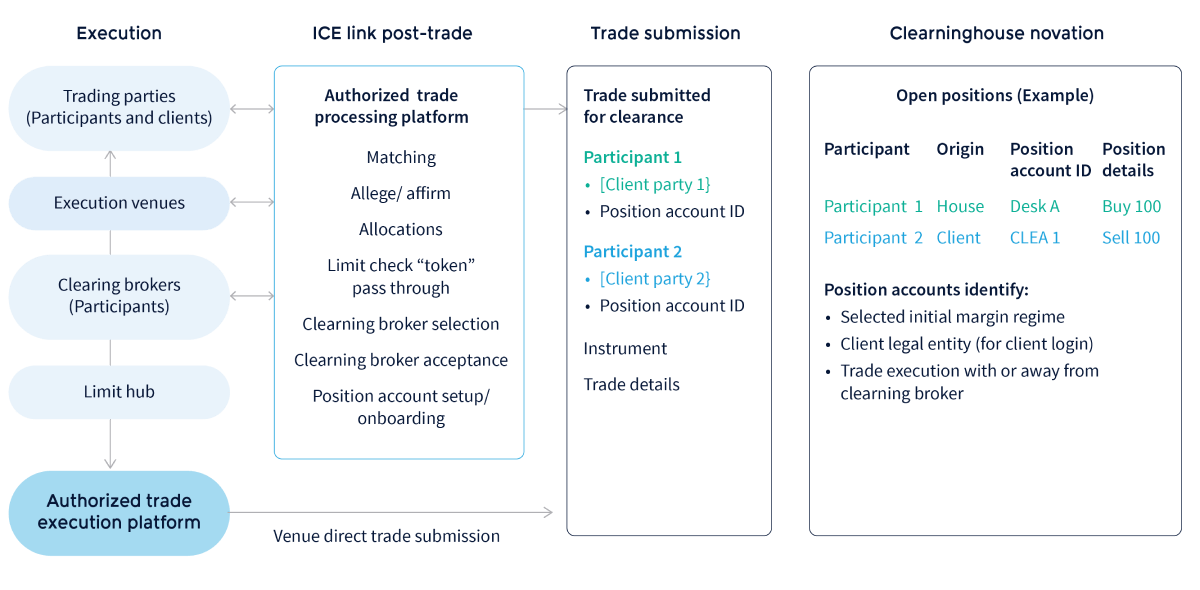

Diagram 1: ICC TCS trade submission and novation. Source: ICC UST Clearing Overview – September 2025.

Diagram 1: ICC TCS trade submission and novation. Source: ICC UST Clearing Overview – September 2025.Diagram 1 shows that trade execution platforms may submit UST trades directly to ICC, if they are pre-authorized to do so for both parties on the trade. Off-venue UST trades may be submitted via ICE Link by market participants, including voice trading parties, repo desks, and clearing brokers. ICE Link matches and affirms the trade (among other functions noted in the diagram) before sending it to ICC.

The trade between two parties is novated to ICC, which replaces the trade with two trades, one between ICE and each of the original trade parties. The two parties are each identified by an account identification (ID). This includes a participant name, a client party name, and a position account ID as illustrated. These can be formatted in two ways:

- Dealer-style account ID: Used when the party is a clearing participant (as for participant 1 in Diagram 1). Participant 1 is the clearing participant’s name. Client party 1 is blank. The position account ID is an account within the house account of the named clearing participant.

- Client-style account ID: Used when the party clears via a clearing broker (as for participant 2 in Diagram 1). Participant 2 is the name of the clearing broker. Client part 2 is the name of the client. The position account is the client-specific account within the overall client account of the clearing broker.

A dealer-to-dealer (D2D) trade (between dealing desks at two banks that are clearing participants) will have a dealer-style account ID in both account IDs.

A dealer-to-client (D2C) trade (between the dealing desk of a bank clearing participant and a client that clears via a clearing broker) will have a dealer-style account ID and client-style account ID (as in Diagram 1).

If the market evolves in this direction, you can see how this protocol could support client-to-client (C2C) trades by having two client-style party IDs.

The above elaboration helps understand ICC handling of done-with and done-away trades. The current norm for clearing D2C UST trades is “done-with” handling, where both sides clear via the dealer’s clearing participant. Here, ICC would require both party IDs to be populated with the same participant name. An emerging alternative D2C clearing approach is “done-away”, where the client has chosen to clear the trade “away” from the dealer. This means the clearing broker is a different clearing participant than the dealer on the trade. ICC would require the client party ID and dealer party ID to be populated with different participant names. Such explicit data capture means ICC UST Clearing needs less variation in processing design to support the distinction between done-away and done-with.

Note also that TCS tags cleared trades with the limit hub tokens indicating the successful outcome of a pre-trade credit-limit check. This supports the needs of parties receiving cleared trades for validation and reporting purposes.

Direct or indirect settlement and delivery

House account margin settlement and trade delivery are always direct. Margin is settled by ICC initiated SWIFT push/pull daily with the pre-funded house origin cash account. Trades are delivered by ICC-orchestrated DVP/RVP between the participant’s securities settlement account and the clearinghouse securities settlement account. Insufficient funds in the dedicated margin accounts to cover the ICC margin requirements would cause failure to settle. After a failure, rapid rectification would be required to avoid immediate defaulting of the participant by ICC. Trade settlement failures remain as unsettled deliver/receive obligations and are processed again the next business day, along with new trade settlements.

Client account margin is always settled indirectly with ICC. ICC initiates SWIFT push/pull daily with the pre-funded client-related cash account of the clearing broker (separate from the house origin cash account). The clearing broker in turn calls margin from the client. This may involve a one-day lag and therefore incur internal credit line usage and funding cost for the clearing broker.

Securities settlement for cleared client trades on a delivery-versus-payment basis can be either direct between ICC and the client, or indirect via a clearing broker as for initial margin (IM) and variation payments. The indirect route is the way things work for credit derivatives trade settlement in ICC. The direct route is there because clients asked for it to enable earlier receipt of securities.

Risk policy and default resources

CCP risk policy includes operational, financial, and risk monitoring controls inherent in the clearing platform and oversight. However, the headline items are the resources set aside for management of participant defaults.

Default resources include:

- “Variation payments”: These are called daily and include variation margin based on the total of changes in open trade present values (PVs), among other components.

- Initial margin (IM): This is based on a “99%-VaR” IM model with a two-day “margin period of risk” (MPOR).

- Guaranty fund (GF): Participant GF contributions are based on a “cover-2” style calculation, driven by the open trade portfolios of the participant and their clearing clients, subject to a minimum of $20 million per participant.

- ICC’s skin-in-the-game (SITG) own capital. The amount is set at $100 million.

Any losses incurred during default close out are covered by default resources in the following “waterfall” order:

- Defaulter’s IM.

- Defaulter’s GF contributions.

- ICC SITG.

- Non-defaulters’ GF contributions.

- End-of-waterfall arrangements.

I have not explored the details of IM and GF calculations or the end of waterfall arrangements. However, the descriptions in the TCS documentation show a structural approach similar to the risk policy and default resources for their existing credit derivatives clearing service.

In the early days of Dodd-Frank and EMIR, ICC’s reputation for solid risk management was helped by the fact that they took an early position on putting SITG before non-defaulters’ GF contributions in their default waterfall. This gave participants the comfort that only an exceptionally large default would burn through the ICC SITG to the non-defaulting participant’s GF contributions and beyond.

Client segregation models

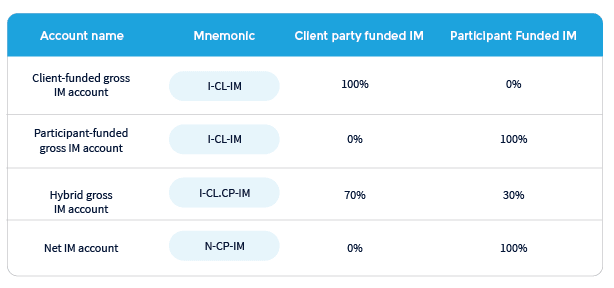

ICC offers more client segregation choices in TCS than they offer for their credit derivatives service, since regulations allow a wider variety of approaches. CFTC regulations oblige OTC derivatives CCPs and clearing brokers to use the LSOC (legally separate, operationally comingled) approach. LSOC forces client-funded gross IM calculation, and segregation by fund or legal entity. This approach corresponds to ICC UST Clearing’s Client-Funded Gross IM Account shown in the first row of the grid below.

Gross IM means the clearing broker pays or passes on the sum of the IM determined separately for each client legal entity or fund, which is therefore not usually exposed to loss from default of another clearing client.

The IM related to each client legal entity is not exposed to loss from the default of another clearing client. When agreeing to incur gross IM at client legal entity level, clients may agree to use one of the three account types in the first three rows of the grid above. These vary only in the split of funding the IM amount, as outlined in the grid.

The last row of the table illustrates the net IM account. Here, the clearing broker Net IM requirement is computed by calculating IM net across all the client portfolios cleared to one Net IM account. The Net IM requirement is generally lower than the sum of the Gross IM requirements for each client portfolio included. However, the collateral on deposit with the clearinghouse related to the Net IM requirement can be used to cure the default of any client using the Net IM account. This exposes each client using a Net IM account to fellow customer risk.

The participant (not the client) pays all IM and variation payments calculated on a net basis across all the client entities having a net IM account. It is for the participant to choose how or even whether to calculate and recoup variation and IM from each client using a net IM account.

Default management

ICC always calls, manages the close-out of, and is solely exposed to, losses from clearing participant defaults. Clearing brokers always call, and are solely exposed to, losses from clearing client defaults. However, clearing brokers can choose to manage a client default close-out themselves or let the clearinghouse manage it on their behalf.

Clearing participant defaults require the close-out of the house account portfolios. They also require the tackling of any clearing clients the defaulting participant may have by porting their entire portfolios to clearing arrangements with willing clearing brokers.

Close-out of a defaulting clearing participant’s portfolio requires ICC to meet the settlement obligations of the defaulting clearing participant. They must also liquidate, via auction or otherwise, the unsettled cleared trades of the defaulting participant, covering any losses incurred using the default resources in the prescribed waterfall order. Generally, T+1 settling cash trades, overnight repos, and term repos close to maturity may be settled by the clearinghouse on behalf of the defaulting clearing participant. Liquidation via auction would be most relevant for term repos with more than a couple of days to maturity. The list of auction bidders is expected to include ICC TCS participants and other bidders by prior arrangement.

Close-out of a clearing client’s portfolio requires the clearing broker to step into all the client’s trades, usually with the help of the firm’s cash and repo trading desks. The trades would be settled, hedged, or sold to other parties. If the clearing broker requests that the clearinghouse manage the default of its client, ICC settles and closes-out the positions using client TCS IM to cover losses incurred.

Approach summary

- ICE chose to build TCS in the ICE Clear Credit (ICC) legal entity, rather than in a separate new legal entity.

- Executed UST trades can be submitted for clearing to ICC direct by multilateral trading platforms, or indirect via ICE Link by market participants, including voice trading parties, repo desks, and clearing brokers.

- The distinction between “done-away” and “done-with” client cleared trades is made by specifying the clearing participant on both sides of the trade submitted.

- Pre-trade credit limit checking is supported by tagging cleared trades with the limit hub tokens indicating the success of the pre-trade check.

- Clearing client trade delivery versus payment can be either direct between ICC and the client, or indirect as for initial margin (IM) and variation.

- Clients always settle IM and variation payments indirectly – first, between ICC and clearing broker, and then between clearing broker and client.

- Funded default resources for TCS are separate from those for credit clearing. They are structured similarly to those of ICC’s credit derivatives clearing service, in waterfall order: defaulter’s IM, defaulter’s guaranty fund contributions (GFC), ICC skin-in-the-game (SITG) capital, and non-defaulters’ GFC.

- Clearing broker and client agree whether the client will clear via a Net IM account (comingled with other entities) or a Gross IM account (mimicking the CFTC LSOC approach).

- Gross IM may be paid by the client or the clearing broker, or split 70:30 between client and clearing broker.

- The clearing broker pays Net IM.

- ICC calls clearing participant defaults and is solely exposed to losses from them. It manages participant portfolio close-out and any porting of client portfolios.

- The clearing broker calls clearing client defaults and is solely exposed to losses from them. It manages close-out itself or asks ICC to manage close-out on its behalf.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.