DTCC clearing mandate survey shows fourfold GSD margin increases

Key Takeaways

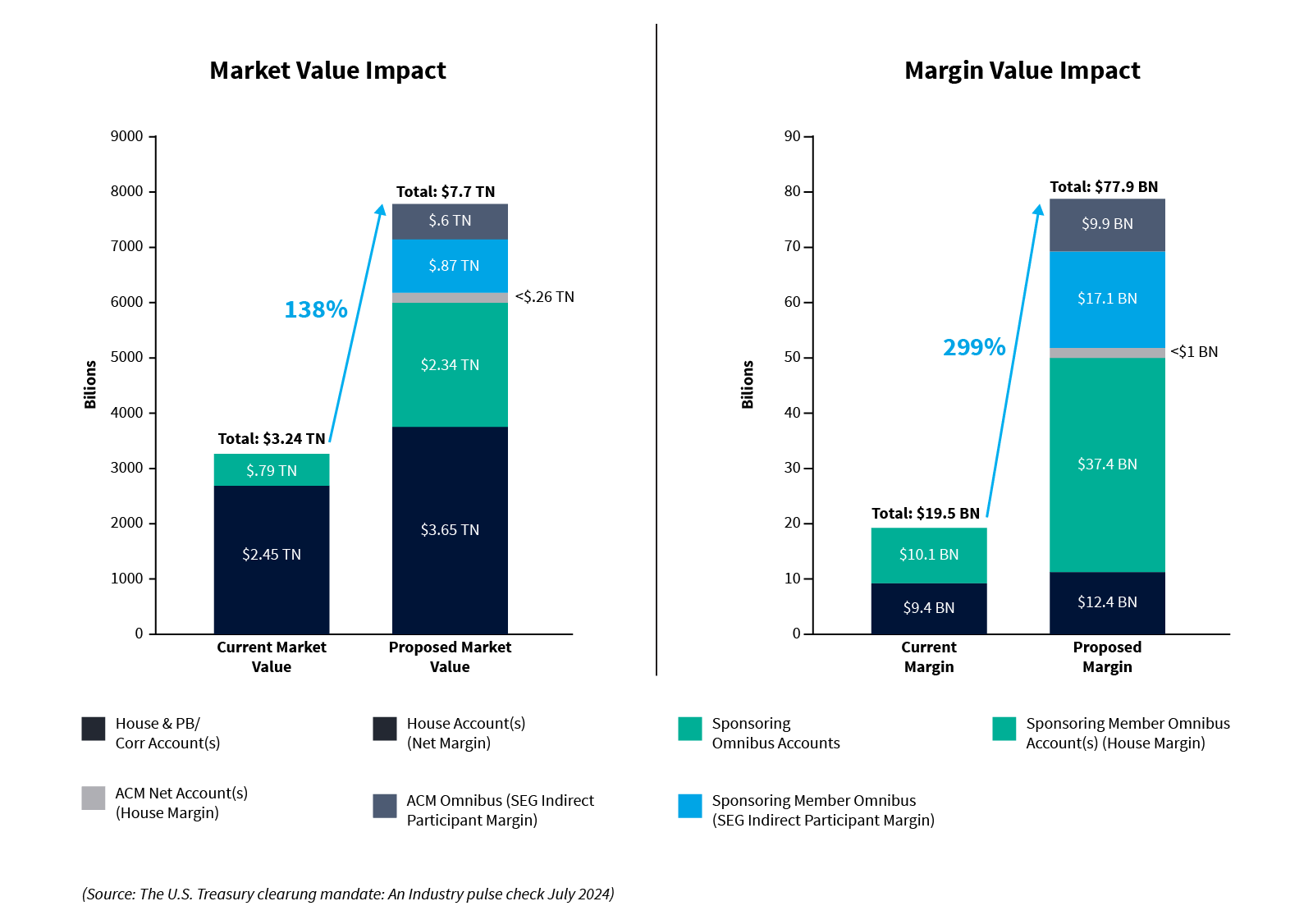

- Post-mandate FICC UST clearing volumes of USD 7.7tn daily and margin of USD 77.9bn – materially bigger than 2023 survey estimates

- Indirect clearing becomes the majority of UST clearing activity and margin

- Sponsored clearing remains the favored indirect clearing choice with rising interest in done-away and agent clearing

In July, DTCC published “The U.S. Treasury Clearing Mandate: An Industry Pulse Check”. Based on a voluntary response survey of GSD (Government Securities Division) netting members, the report aims to summarize big banks’ current perspective on the impact of the SEC UST clearing mandate at go-live in mid-2026.

Post-mandate volumes and margin estimates

The big story in the report is in the chart copied over from section 4:

(Source: The U.S. Treasury Clearing Mandate: An Industry Pulse Check July 2024)

(Source: The U.S. Treasury Clearing Mandate: An Industry Pulse Check July 2024)From current (mid-2024) to proposed (mid-2026), the report estimates:

- Total clearing (all bars) increases substantially: activity up USD 4.46tn to USD 7.7tn (2.4x) and margin up USD 58.4bn to USD 77.9bn (4.0x)

- Direct clearing (dark green bars) increases moderately: activity up USD 1.40tn to USD 3.85tn (1.5x), margin up USD 3.0bn to USD 12.4bn (1.3x)

- Indirect clearing (the sum of the other color bars) becomes the majority: activity up USD 3.26tn to USD 4.05tn (5.1x) and margin up USD 55.4bn to USD 65.5bn (6.5x), which splits into member-paid USD 37.4bn (pale green bar) and client-paid USD 27.0bn (the top two orange bars)

Direct clearing’s moderate increase is partly explained by Section 6 of the report. This shows only 30% of responding banks expect to onboard one or more group entities as new netting members, while 57% expect to onboard one or more group entities to indirect clearing. We would also note that the clearing mandate inter-affiliate exemption enables bank entities to avoid FICC clearing. Instead, they can trade back-to-back with their affiliated netting member which simultaneously executes the street trade.

The large increase in indirect clearing indicates that, despite recent surges, most of the client activity (as well as bank non-netting member affiliate activity) is still to transition.

One number sticks out: the USD 37.4bn of bank-paid margin on client-driven indirect clearing (pale green bars). We would be surprised if banks rolled over and paid this without getting most clients to pay it back – either by moving to seg margin or, at a minimum, paying back the interest cost. Therefore, we have mentally noted the total indirect clearing margin of USD 65.5bn and placed an asterisk against who will pay the costs.

The basis of the estimates

The introduction notes that about half (83 of 167) of the netting member entities responded. Though this seems limited, most of the primary dealers and some of all participant types responded. Therefore, most of the activity is likely represented, and the report is credible.

At about this stage of the OTC clearing mandate, back in the day, a bank or client trade association or two overestimated the required OTC IM. These estimates had not allowed for the creation and adoption of margin efficiency tools to reduce trading costs. On the other hand, their estimates served to point out the broad scale of the increase. Expecting similar behavior here, we think the estimates require, say, a 20% haircut but are not an unreasonable guide to the outcome.

Margin efficiency tools

Such big margin amounts suggest banks and clients will be creative in finding efficiencies. The report mentions several tools which can help:

- Agent clearing margin netting. The report indicates increasing interest in agent clearing, which can be done with margin netting, unlike sponsored clearing – the current leading indirect clearing method – which is usually margined gross by client fund entity. The report hints at open bank interpretation discussions which may ameliorate the bank capital usage and credit exposure downsides, which we had previously assumed were holding agent clearing back.

- Done-away clearing. The report notes growing interest in enabling clients to trade done-away with any dealer without having an indirect clearing arrangement with that dealer. Instead, they give up the trade to a single member clearing provider, thus consolidating to a single cleared portfolio, and netting down margin.

- CME-FICC portfolio margin. After some set-up and legal documentation, partial risk offsets are allowed between FICC repo and CME IR futures and options portfolios – netting down and reducing the aggregate margin. The report mentions FICC is looking to expand this capability to indirect clearing accounts.

We would add other tools not mentioned in the report:

- Inter-affiliate trading, in which banks use the inter-affiliate trade clearing exemption to consolidate external repo trades of the group in a single margin-efficient netting member account.

- Bank portfolio margin, which would allow a client to net their trades with a specific bank across client-cleared and uncleared and across repo and interest rate derivatives, but we are unclear whether banks have succeeded in including cleared repo.

- CCIT membership, which would allow money funds to clear margin-free, but SEC has yet to approve.

- Guaranteed repo, which would be margin-free uncleared client-to-client repo but has yet to take off.

The DTCC report and the numbers highlighted above show substantially increased FICC UST clearing activity and margin funding costs for UST trading participants by end-2026.

Bank-to-client negotiations of trading and indirect clearing arrangements may become interesting as indirect clearing pricing of margin and capital costs standardizes and margin-free alternatives, perhaps, gain traction.

We aim to compare the economics of the various tools and approaches in more detail in a future post. Watch this space!

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.