Can US buyside firms eliminate UST repo cleared margin for some trades?

Key Takeaways

- The SEC UST clearing mandate makes buyside funds pay most of an estimated USD 55 billion increase in FICC indirect clearing margin by mid-2026

- If set-up challenges can be overcome, both uncleared guaranteed DVP and triparty repos and direct CCIT member cleared triparty repos have no cleared margin

As covered in our recent blog, the DTCC’s recent FICC GSD member survey estimated a USD 55 billion increase in indirect clearing margin by the mid-2026 go-live of the SEC UST clearing mandate. This compares with only a USD 3 billion estimated increase in direct participant clearing margin.

Given there is no required margin on uncleared UST repo, USD 55 billion is a big funding increase. It suggests most buy-side firms’ UST repo activity has yet to shift to clearing. As outlined in the blog linked above, funds can reduce margin costs using portfolio netting tools. Here, however, we look at two ways to eliminate altogether the cleared margin on a trade:

- Cash-lender-only money funds can become a Centrally Cleared Institutional Triparty (CCIT) member for triparty trades

- Any fund can trade guaranteed repo for triparty or DVP (delivery-versus-payment) trades

Relevant costs

Margin costs include the burden of funding to be raised and the interest cost incurred. Indirect cleared trades incur margin directly on the client fund’s seg margin account or indirectly on the client account within the netting member omnibus account, the costs of which we assume will be passed on to the client fund in clearing sponsor charges.

Regulatory capital costs take the form of ccRWA (counterparty credit risk weighted assets) usage on the counterparty default exposures of a bank. We assume the costs of this will be passed on to the client fund in the cases considered as guaranteed repo fees or clearing sponsor charges. For brevity, we ignore the tiny bank leverage costs involved in guarantees.

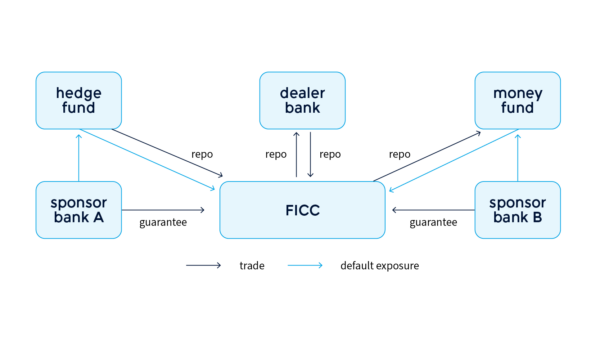

Cleared repo

The client-to-client repo shown is intermediated by a single dealer bank as principal and sponsored cleared on both sides. This results in four FICC cleared repos. Each sponsored cleared repo requires a client settlement guarantee from the sponsor bank to FICC (Fixed Income Clearing Corp.), which results in sponsor bank default exposure to the client fund.

Dealer bank cleared repo costs can be treated as minimal given VAR netting of equal and opposite trades in margin calculation and QCCP (qualifying central counterparty) risk weights of 2% in the bank’s ccRWA calculation.

The costs of each fund repo are:

- Margin

- Sponsor bank ccRWA on the default exposure to the fund from the guarantee

- Zero sponsor bank leverage or ccRWA on the repo, since the sponsor bank is not principal to the repo

Since it is exclusively a cash lender, the money fund can use direct CCIT membership clearing instead of indirect sponsored clearing for triparty (but not DVP) trades. No margin is now incurred because instead FICC takes recourse in default to the cash lent by the fund. No ccRWA is now incurred as no sponsor bank is involved in the client-cleared leg.

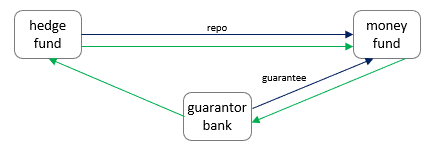

Guaranteed repo

A guaranteed repo comprises a client-to-client repo booked and settled direct between the funds (with help from the vendor settlement partner) and a guarantee of hedge fund settlement provided to the money fund by a guarantor bank on which the bank has default exposure to the hedge fund. Two questions are worth covering off:

- How can the money fund trade with the hedge fund? Because the guarantee replaces an unacceptable hedge fund default exposure with an acceptable bank default exposure.

- Why is the repo not mandated to clear? Because no direct clearing participant bank is principal to the repo.

The costs are:

- Zero margin (not required on uncleared trades)

- Guarantor bank ccRWA on the guarantee (based on the hedge fund exposure)

- Zero guarantor bank leverage or ccRWA on the repo, since the guarantor bank is not principal to the repo

Trade level incentives

A US hedge fund (trading DVP or triparty) is incentivized to choose guaranteed repo by the cleared margin.

A US money fund trading DVP will be incentivized to choose guaranteed repo by margin and possibly by guarantee fees reflecting no ccRWA.

A US money fund trading triparty may eliminate both margin and bank ccRWA using either CCIT membership clearing or guaranteed repo. It will decide “at trade” based on available liquidity and relative pricing.

Set-up challenges but advantages are clear

CCIT membership is live with some activity at FICC but not approved by SEC for use by registered investment companies (RICs), which prevents most money funds using it. Just like under sponsored clearing, under the direct CCIT model the money fund must settle direct with FICC, but there is no margin processing and no sponsor settlement guarantee. This suggests money fund infrastructure set-up costs will be relatively small. The main challenge is for money funds to convince the SEC to approve CCIT for RICs.

Guaranteed repo requires one or both vendor platforms (Sunthay, Venturi) to get going. In turn, this requires participant funds and dealers to make changes to their trading and processing infrastructure. Adequate payback on the largely fixed costs of those changes will require a material slice of total activity to shift to guaranteed repo.

For client UST repo, guaranteed repo and CCIT membership offer to eliminate some of the margin and ccRWA costs of sponsored clearing.

The financial cost advantages are clear but can funds and banks overcome the set-up challenges outlined?

As always, we welcome comments and questions.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.