SEC Proposal to Mandate Climate Risk Disclosures

Sustainability is a contentious topic in the US, and the Securities and Exchange Commission’s (SEC) climate disclosure rule for listed companies is no exception. It is not only widening the political divide across the country but also for many industry participants testing the boundaries of securities laws and the commission’s authority.

The larger firms already provide voluntary sustainability reports. The SEC estimates that a third of the 7,000 corporate annual reports it reviewed in 2019 and 2020 included some climate impact disclosures, see the SEC Statement on Proposed Mandatory Climate Risk Disclosures.

However, if given the green light, the new disclosure rule would require a significant change in that companies would have to provide a much more comprehensive annual account of how they assess, measure and manage climate-related risks. In addition, they would need to divulge their governance practices on climate-related risks and relevant risk management processes, see SEC Press Release 2022-46.

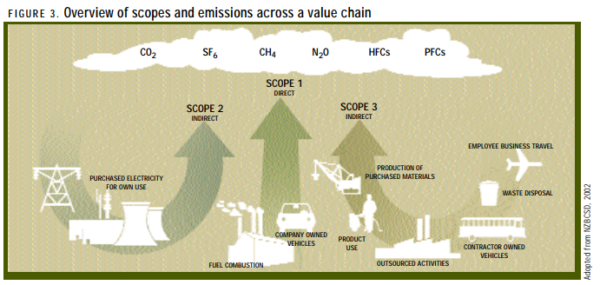

The main benchmark used is the Greenhouse Gas (GHG) Protocol and Scopes 1, 2 and 3. The first two involve companies disclosing the direct impact of their operations on climate change in terms of the products they make and any indirect effects on the environment that come with using electricity, trucks or other vehicles. The third and most extensive and contentious is evaluating the carbon footprint of suppliers, business travel and any assets a company leases.

Scope 3 is considered the most contentious because of the mammoth task of collecting and analyzing the data, and the compliance costs involved. These concerns are reflected in the comment note from the US Chamber of Commerce, the largest business lobbying group in the country, which called this category a “massively burdensome undertaking.”

Opponents also argue that the greater transparency requirement would hold companies accountable for their role in climate change, and perhaps encourage investors to exert more influence in forcing firms to alter business practices. Moreover, there are questions about whether the SEC has overstepped its legislative reach. Republican attorney generals from 24 states believe the SEC does not have the mandate to implement the rules.

They contend that the SEC should stay within its remit, written over a century ago, which states “that legitimate mandatory disclosures are those required to protect investors from inflated prices and fraud, not merely helpful for investors interested in companies with corporate practices consistent with federally encouraged social views.” (Mayer Brown article).

SEC Commissioner Hester Pierce shares their views in her dissent opinion, she questioned whether the agency had the power to prescribe such extensive rules that are intended to manage the economy and businesses. As she succinctly put it “We are not the Securities and Environment Agency – at least not yet.”

Those in favor of the rule counter the criticisms by noting that the disclosure rules will give investors a clearer picture of the risks that climate change might pose to listed companies, especially given the increase in natural disasters as well as changes in government environmental policies or consumers’ reticence in buying products that contribute to global warming.

In his recent testimony to the Committee on Banking, Housing and Urban Affairs, SEC chair Gary Gensler, reaffirmed that the SEC was indeed within its mandate. He said, “This is built on multidecades of authority about disclosure. We have no climate agenda whatsoever.”

However, the comments received have already caused a delay in finalizing the rule. The target deadline for the 490-page tome was October 2022. Given the debates, discussions and consultations, this was pushed to October 2023, with an effective implementation date of 1 January 2024.

The jury is out as to whether the rule will see the light of day at the beginning of next year. At the hearing, Gensler declined to give a timeline. “I don’t want to be pinned down on this one,” he said. “There is a very heavy comment file, and some really important issues have been raised. We try not to do things against a clock.”

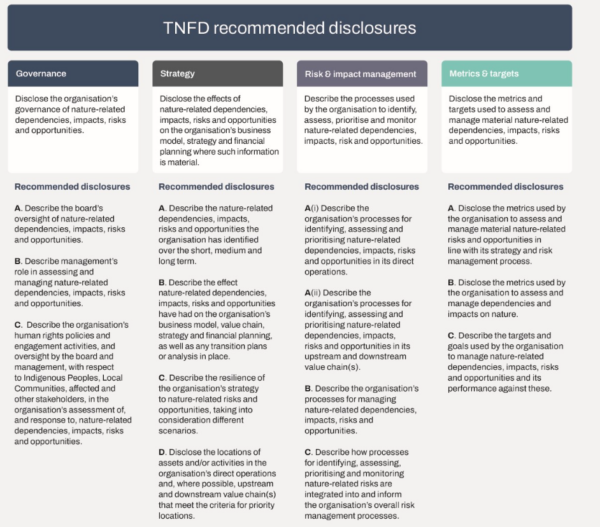

The rules are based on international standards so even if there are further delays, US companies may be obliged to report climate risks to some degree under IFRS S2 Climate-related Disclosures and the Task Force on Nature-related Financial Disclosures, which just issued its final recommendations.

The US will also be out of step with Europe which is at the forefront of climate regulation and recently adopted the European Sustainability Reporting Standards and the Corporate Sustainability Reporting Directive.

In the end though, it could be the investors who have the final vote. Despite the political ructions and questions over the SEC’s reach, there is a growing demand for greater transparency and detailed information about a company’s climate risks. If they are absent, then they may turn to greener pastures.