The MiFID II Review – the Market Model Typology (MMT) post-trade data standard

For more on the MiFID II Review, see part one of our series.

In 2018, regulators intervened to improve post-trade information with MiFID II. Their aims were to:

- Improve the quality and consistency of raw data. This was to be achieved through more standardized trade reports, and OTC trade reporting through an APA (Approved Publication Arrangement).

- Reduce the cost of post-trade data for investors, including the unbundling of pre- and post-trade data, and the introduction of a European Consolidated Tape.

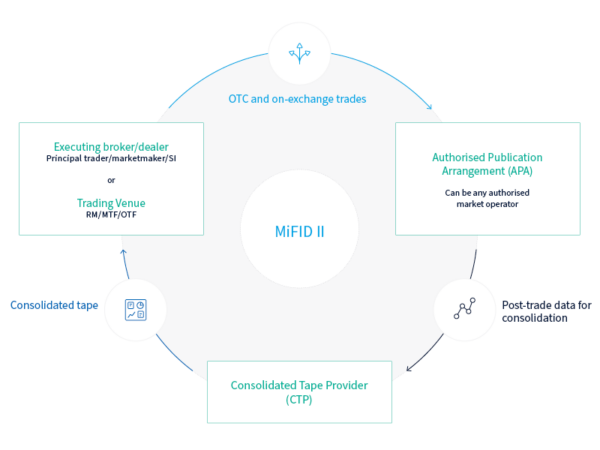

To help achieve these objectives, new APA and CTP (consolidated tape provider) entities were introduced. ESMA also promised to develop common formats, data standards, and technical arrangements, to streamline post-trade data consolidation.

What does the consolidated tape requirement mean for the markets?

MiFID II called for consolidated post-trade data to be available for all EU instruments (including those traded off exchange). Rather than participants having to consolidate this data from numerous sources themselves, data would be available as a single consolidated tape. To achieve the goal of a single consolidated tape, markets and regulators need to agree on a standard format for trade data across all EU venues.

Current regulatory developments – improving standardization and transparency.

Improving transparency is again a key goal for the upcoming round of rules adjustments, aka the MiFID II Review, including further efforts to establish a consolidated tape. Better data quality is a prerequisite for any tape and represents one of the main challenges and costs of implementation. More standardization of data across trading venues is also required. However, a common standard has already been developed, one which many trading venues already adhere to. This is the industry-led Market Model Typology initiative (MMT).

The MMT standard

The MMT standard covers post-trade data across all asset classes subject to MiFID II. It is a collaborative initiative, established by industry participants to improve the quality of post-trade data with standards for post-trade transparency. The MMT was originally built on some earlier advice from ESMA’s predecessor CESR (the Committee of European Securities Regulators, replaced in 2011). MMT introduces a standard set of codes, making it easier for investors to compare and consolidate market data. The MMT industry standard effectively maps legacy trade (reporting) flags to a common code.

Over recent years, the MMT has gained industry support and broad implementation across Europe, moving under the jurisdiction of the FIX Protocol Limited Trust (Trust) in 2013. Regulators are aware of the MMT standard, having referenced it in the current review of MiFID II, indicating support of adoption.

MMT takes the form of a data model and cross-reference table. Trade flags from venues (such as securities exchanges, MTFs, and OTC reporting destinations) are mapped to a set of standard single character enumerations (the native code includes 14 characters). MMT is endorsed by trading platforms and reporting venues, as well as the major market data vendors and other market participants. The latest version of MMT (4.0) is due to launch in 2023. This upgrade covers changes to RTS 1 and RTS 2 of MiFID II/MiFIR, which will apply from 1st January 2024.

MMT continues to gain approval across the industry. However, it is not yet clear what impact it will have on the development of a consolidated tape. To avoid reinventing the wheel, industry stakeholders need to remain engaged with the regulatory process and industry-led initiatives.

Regulation matters

To tap into ION Markets’ views and commentary on the upcoming MiFID II review, and other emerging financial regulation please subscribe to our blog.