Virtual account management – visibility, control, and efficiency

What is a virtual account? Why do banks offer them to their corporate customers and why do these corporates want them?

In this blog post, we discuss the motives for using and offering virtual account management solutions. We begin by answering the first question.

What is a virtual account?

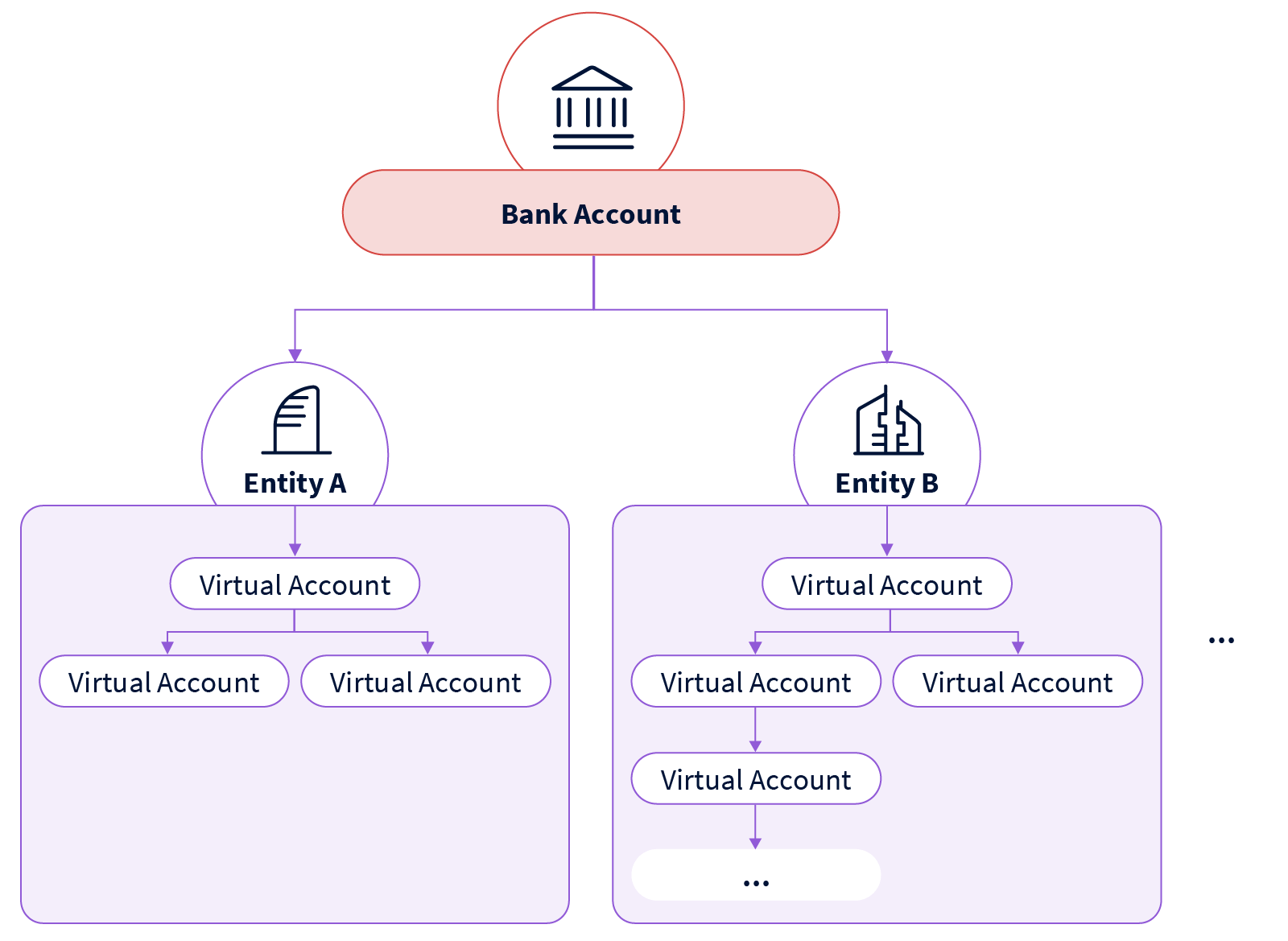

A virtual account is linked to a “real” or “physical” bank account. Transactions on these are booked on both the virtual account and the real account. So, virtual accounts can be considered as a “subledger” of the real bank account. Another defining feature of a virtual account is its “virtual bank account number”. This number allows a virtual account to be identified uniquely and to receive or initiate payments – just like real bank accounts. Many virtual accounts can be assigned to a single real bank account. As such, the real account acts as the top layer of a structure, which can be layered on multiple levels.

Benefits of a VAM solution

Virtual account management (VAM) gives corporate treasurers the flexibility to adapt their own bank account structures according to their changing business needs. VAM propositions provide the following benefits to corporate treasurers:

- Visibility: As transactions are assigned to their respective virtual accounts, corporate treasurers have overview and transparency over where their company’s cash is located.

- Multi-entity: Virtual account structures can span multiple entities.

- Flexibility: Given that a defined “band” of virtual account numbers is typically provided by banks, opening new virtual accounts is a quick and efficient process to replicate the corporates’ underlying business.

- Self-service: Self-servicing options for corporate customers allow fast and safe changing of product details – without having to involve the bank.

- Reconciliation efficiency: Inbound transactions can be identified uniquely as they are directly booked onto a virtual account. This leads to increased reconciliation efficiency.

- Automatic centralization: Cash is centralized automatically, as transactions are also booked onto the real bank account. This type of “cash pool” can be cheaper than running a dedicated cash pool with real accounts. Using this approach, virtual accounts might provide corporates with cost savings.

- In-house banking: VAM solutions also provide In-house Banking functionalities – like interest calculation capabilities, or payment initiation.

As banks offer bank account services, they are also well positioned to provide VAM solutions to their corporate customers. The following benefits arise for banks offering VAM services:

- Customer retention: Corporate customers demand VAM solutions due to the discussed advantages. Banks respond by supplying VAM services.

- Increase revenue: With an attractive VAM offering, banks can increase their revenue by winning new clients.

- Reduced costs: Self-servicing options for corporate customers can reduce administrative efforts, as bank employees need to do fewer tasks.

VAM supports liquidity management

VAM systems support features revolving around tracking transactions and balances on virtual accounts. Typically, this enables liquidity management functions like:

- Cash visibility: The distribution of a real bank account’s balance across different virtual accounts provides corporate treasurers with mission-critical information on where funds are allocated.

- Account reports can be handled like “bank statements”. They can be generated for virtual accounts in typical formats such as MT940/MT942 or camt.053/camt.052. This facilitates treating a virtual account as “just another bank account” in corporate customers’ ERP systems.

- Payments can be initiated out of a virtual account, further bolstering their usefulness in liquidity management.

- Interest calculations can be performed for virtual accounts, enabling in-house banking applications within virtual account solutions. The calculations can be differentiated by entity/ per virtual account.

- Structure maintenance: A VAM solution typically has self-service capabilities. Corporate customer users can manage the activation/deactivation of virtual accounts on their own, thus providing them with the tools to solve challenges in liquidity management and transaction reconciliation.

Lifecycle of a transaction

The typical lifecycle of a transaction within a VAM ecosystem is as follows:

- A bank’s corporate VAM customer creates a virtual account for one of their frequent buyers.

- The buyer then uses a specific virtual bank account number to settle outstanding bills. This number cannot be distinguished from a non-VAM bank account number.

- The buyer instructs a payment to the given virtual bank account number.

- The bank running the VAM solution receives the payment. The bank’s (payment) system detects that the payment target is a virtual account.

- The payment is routed to the virtual account and the corresponding real bank account – updating both balances at the same time.

- The bank’s corporate VAM customer sees that the payment was received and can designate the payment immediately to the specific buyer.

VAM at Reval Treasury Services

Reval Treasury Services is a comprehensive application allowing banks to provide liquidity management services – ranging from cash concentration to cash flow forecasting to their corporate customers. It helps banks offer a virtual accounts solution by combining VAM capabilities, bank integration, and a customer user interface with self-service options.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.