The dynamic risk management model in hedge accounting

Dynamic risk management (DRM) is a new proposed model for hedge accounting within IFRS. It differs from the current hedge accounting methodology for interest rate portfolio of hedges and is expected to bring hedge accounting closer to an entity’s risk management practices

Concepts of dynamic risk management

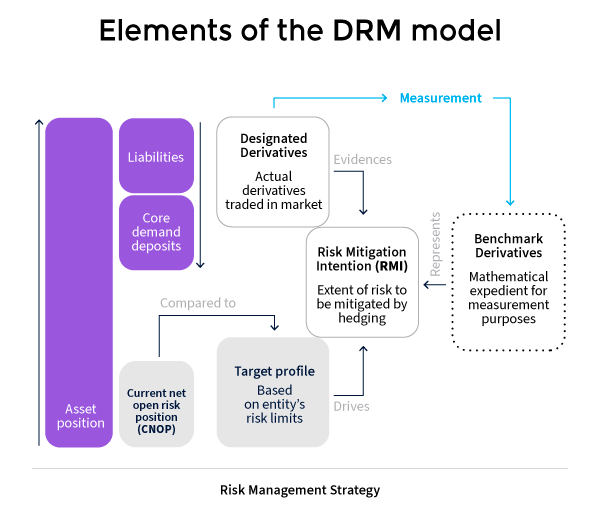

Recently, the International Accounting Standards Board (IASB) and others shared their initial thoughts on the model [1], [2]. DRM has several main building blocks:

- An open portfolio of transactions – the so-called current net open risk position (CNOP).

- The external derivatives hedging CNOP.

- Target profile (TP) and risk mitigation intention (RMI) used for the hedge assessment, qualification, and measurement.

CNOP is the net of the actual and forecast assets, liabilities, and demand deposits in a portfolio of transactions traded by the entity’s front-office [3]. CNOP is associated with its risk terms, for example, with PV01 of the portfolio.

Risk managers decide on hedging the CNOP with externally traded derivatives. They may not hedge the CNOP in full – the difference is the residual open risk position.

The accounting policy specifies a TP as a range of risk limits (represented by PV01) that are acceptable for CNOP combined with hedging derivatives. That is, the acceptable PV01 range for the Residual open risk position.

Further, hedge accountants model benchmark hedging derivatives (hypotheticals) so that they match the PV01 of external derivatives at inception. The PV01 of these hypotheticals and its time evolution represent the RMI. This is used for ongoing measurement of ineffectiveness.

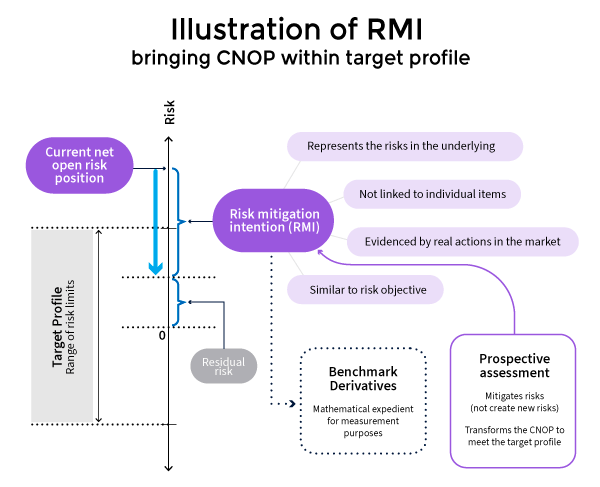

In general, TP and RMI are set by period (time bucket) and may differ period by period. At every period end, PV01 of the CNOP is evaluated and compared to RMI (PV01 of benchmark derivatives at the period end). Retrospective assessment determines whether the CNOP combined with the TMI is within the TP – as shown in the next figure 1. Failures may be due, for example, to unexpected changes in CNOP, and imply a de-designation action.

The period-end measurement compares RMI to the designated external derivatives. This comparison determines the aligned (with RMI) and misaligned portions of those external derivatives. The fair value of the designated externally traded derivatives is then split: the aligned part is posted to the “DRM adjustment” account – a separate line item within OCI on the balance sheet. The misaligned part is recognized in the P&L.

This DRM approach replaces the concepts of IFRS9, namely hedged risk, designation of individual transactions, and applying effectiveness assessment calculations on the fair value changes of transactions.

The hedged items that qualify for inclusion in CNOP and, therefore, in the DRM hedge relations are assets and liabilities accounted for at amortized cost (AC), or – for financial assets – at fair value through OCI. Assets or liabilities measured at fair value through the P&L, or already designated in other non-DRM hedge accounting relationships, cannot be designated in the DRM model.

DRM is still “under construction”. The exposure draft is due in 2025, and the effective date is expected in 2028. The details, including those outlined in this article, may still change. However, the main idea – that is, to bring the hedge accounting model closer to risk management frameworks – is set.

Preparation for the dynamic risk management accounting model

At ION, we closely follow developments of the accounting standards. This includes the DRM model. Our goal is to understand its applicability across the industry segments and, therefore, the impact on the ION’s TMS solutions.

ION’s HATT team – comprising hedge accounting experts across ION’s TMS solutions – is available to answer questions related to the DRM developments. To speak to the HATT team, talk to your ION account manager about arranging a call.

References:

[2] https://www.isda.org/a/Hl1gE/Preparing-for-the-Dynamic-Risk-Management-Accounting-Model.pdf

[3] While DRM is an activity-based and not industry-based model, IASB expects that banks and possibly the insurance industry do engage in the related risk management practices. Therefore, they will be among the first adopters of the DRM model. https://www.ifrs.org/content/dam/ifrs/meetings/2024/july/iasb/ap4a-applicable-risk-management-activities-drm-model.pdf

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.