ASC 815 portfolio layer method: Unveiling its functionality, benefits, and considerations

FASB ASC 815 guides entities on accounting for derivatives and hedging activities. In 2022, FASB issued a regulatory update: Accounting Standards Update (ASU) No. 2022-01, Derivatives and Hedging (Topic 815): Fair Value Hedging — Portfolio Layer Method (PLM).

The “portfolio layer” method, originally known as the “last-of-layer” model, introduces a distinctive approach to fair value hedges for reporting entities. It allows entities to designate a specific portion of a closed portfolio as the hedged item. This includes both prepayable and non-prepayable financial assets or beneficial interests. ASU 2022-01 provides enhanced flexibility, empowering entities to manage their prepayment risk within the hedge relationship, irrespective of the portfolio’s composition.

Read this blog post to learn about the benefits, challenges, and opportunities of the new regulatory rules.

Key Benefits of the Portfolio Layer Method

Traditionally, risk managers have adopted a practice of hedging each debt security individually, a method often associated with challenges such as over-hedging. So, there arises the need for de-designation when a hedged item undergoes sale, prepayment, or when issuers default on their debt. The Portfolio Layer Method (PLM) presents a solution to these challenges, enabling risk managers to establish multiple hedging layers.

The PLM offers several key benefits:

- Lower Prepayment Risk: The PLM plays a pivotal role in mitigating prepayment risk for companies. By minimizing the impact of individual underlying transactions on the overall portfolio and hedging strategy, it helps reduce the exposure to prepayment-related uncertainties.

- Increased Control: Entities applying the PLM gain enhanced control over the life cycle of individual portfolio layers. This flexibility allows them to tailor each layer according to the specifics of their debt securities and management plans.

- Improved Hedging Performance: Implementation of the PLM results in a more robust and effective hedging strategy. Its structure reduces susceptibility to ineffectiveness, demanding less oversight from the hedge manager due to its closer resemblance to economic hedging principles.

Portfolio Hedging Strategies

The utilization of the Portfolio Layer Method (PLM) aligns seamlessly with the principles of economic hedging. Economic hedging, which aims to mitigate interest rate or FX risks across an entire portfolio, operates independently of the intricate and often challenging hedge accounting standards.

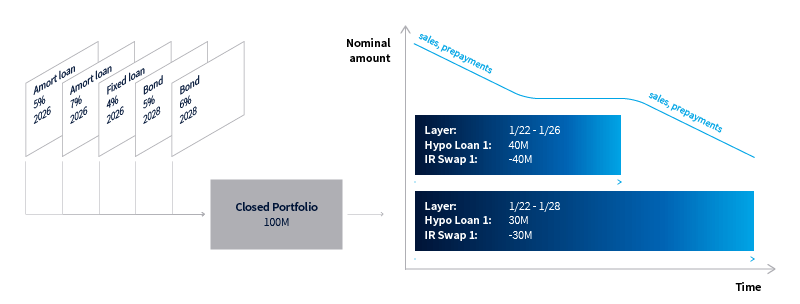

Consider this scenario: An entity manages a closed portfolio comprising diverse debt securities susceptible to later prepayments, defaults, or sales, prompting the decision to implement a hedge. The traditional approach involves individually hedging each security, tailoring derivative transactions to the specifics of each debt security. This needs substantial managerial effort and continuous monitoring, resulting in elevated transaction costs. Moreover, the common occurrence of debt prepayment leads to ineffectiveness and needs frequent de-designation. In essence, managing hedges through this method proves to be both costly and labor-intensive.

The PLM presents an alternative. Risk managers employ a limited number of hypothetical transactions representing the entire closed portfolio. So, only a minimal number of derivative transactions are required to hedge the entire closed portfolio. The risk manager has the flexibility to structure these derivative transactions in two ways: through parallel layers, combining transactions with different maturities, or through sequential layers, allowing for forward-starting transactions.

Parallel Portfolio Layers

All layers commence simultaneously but conclude at distinct future dates. The longest maturity layer supports the outstanding security amount that is likely to persist until the closed portfolio matures. Subsequent layers have shorter maturities, supporting additional available amounts during their respective periods. Multiple layers can be created, each hedged with a derivative mirroring its maturity and opposite amount. The objective is to hedge the maximum outstanding amount during the closed portfolio’s lifecycle.

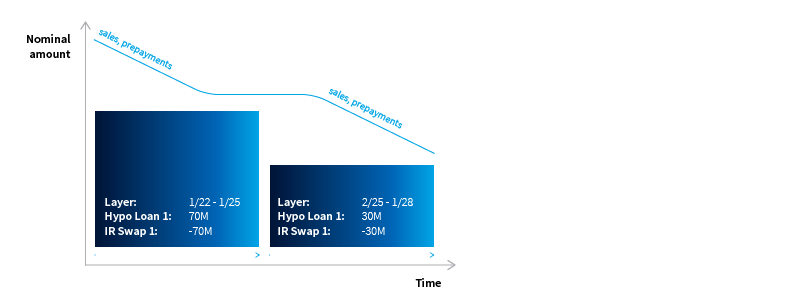

Sequential Portfolio Layers

In this strategy, one layer matures before the commencement of the next. The expected outstanding amount for the entire layer period is hedged. For future-starting layers, forward-starting derivative instruments are employed. Typically, the total debt securities amount is not fully hedged, allowing for adjustments due to prepayments or similar events.

Both portfolio layer strategies provide more flexibility on the derivative side, empowering risk managers to optimize transaction costs.

Considerations before implementing the new standard

While the Portfolio Layer Method (PLM) presents considerable advantages, its implementation needs careful consideration. The expertise of hedge accounting specialists is crucial to meet the demands of new regulatory requirements. It is imperative to scrutinize existing processes and tools to ensure the efficient and secure hedging of closed portfolios.

ION offers tools to automate risk management and hedge accounting processes, coupled with the expertise required for a seamless implementation of new regulations. It assists companies in optimizing cash, liquidity, financial risk, and hedge accounting. The software encompasses robust hedge accounting and valuation capabilities. Also, clients can engage in discussions about their hedging strategies and navigate new regulations with ION’s experts from the Hedge Accounting Technical Taskforce (HATT). Unsurprisingly, ION clients consistently emerge as early adopters of new standards and regulations, such as the ASC 815 Portfolio Layer Method.

In conclusion, the ASC 815 Portfolio Layer Method stands out as an effective hedging strategy, empowering entities to hedge multiple debt securities within their portfolios efficiently. ION’s treasury management systems are adept at supporting this new standard, enabling customers to not only meet regulatory requirements but also apply a more flexible and tailored approach to their hedging strategies.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.