ESMA’s consultation to simplify financial transaction reporting across EMIR, MiFIR, and SFTR

Key Takeaways

- ESMA’s consultation explored two routes to simplify EU transaction reporting.

- Options: streamline existing channels; or build a single, unified system.

- Final report outlining the preferred model is due early 2026.

Europe’s system of financial transaction reporting is set to change. On 23 June, the European Securities and Markets Authority (ESMA) launched a consultation to streamline reporting and reduce compliance burdens without compromising transparency or oversight. Banks, asset managers, market infrastructures, fintech firms, and technology vendors — all key players in collecting and submitting trade data — were invited to share their views by 19 September.

Across Europe, firms juggle a patchwork of reporting regimes, each capturing a different segment of the market:

- MiFIR covers trades in financial instruments, such as shares and bonds.

- EMIR focuses on derivatives, particularly those traded over the counter (OTC).

- SFTR tracks securities financing deals, like repos and stock lending.

- REMIT governs wholesale energy markets, ensuring integrity and transparency in power and gas trading.

The scope depends on a firm’s activities. While large financial institutions active across markets may report under all three financial regimes, smaller firms or sector specialists fall under one or two.

Overseeing the system, ESMA sets the rules and aligns national authorities to keep reporting consistent, and Europe’s markets transparent and well-supervised.

Challenges in EMIR, MiFIR, and SFTR reporting: too many channels, not enough clarity

But, according to ESMA, the system has grown too complex and overlapping. A single trade can trigger multiple reporting obligations under different EU rules, often through separate channels and formats. Each regime uses its own templates, definitions, and technical standards. Therefore, firms often end up resubmitting the same information — from transaction details to instrument reference data that identifies each security or contract. In some cases, firms must report at both the transaction level, capturing individual trades; and at the position level, showing their overall exposures. It all depends on which regulation applies.

The result is a tangle of duplication and inconsistency that drives up firms’ compliance costs and can leave supervisors working with fragmented or unreliable data.

ESMA now aims to resolve this scenario via its simplification initiative.

ESMA’s proposed options for reporting simplification

In its Call for Evidence, ESMA sought industry feedback on two main options — each with possible variations — for simplifying the reporting of financial transactions across the EU.

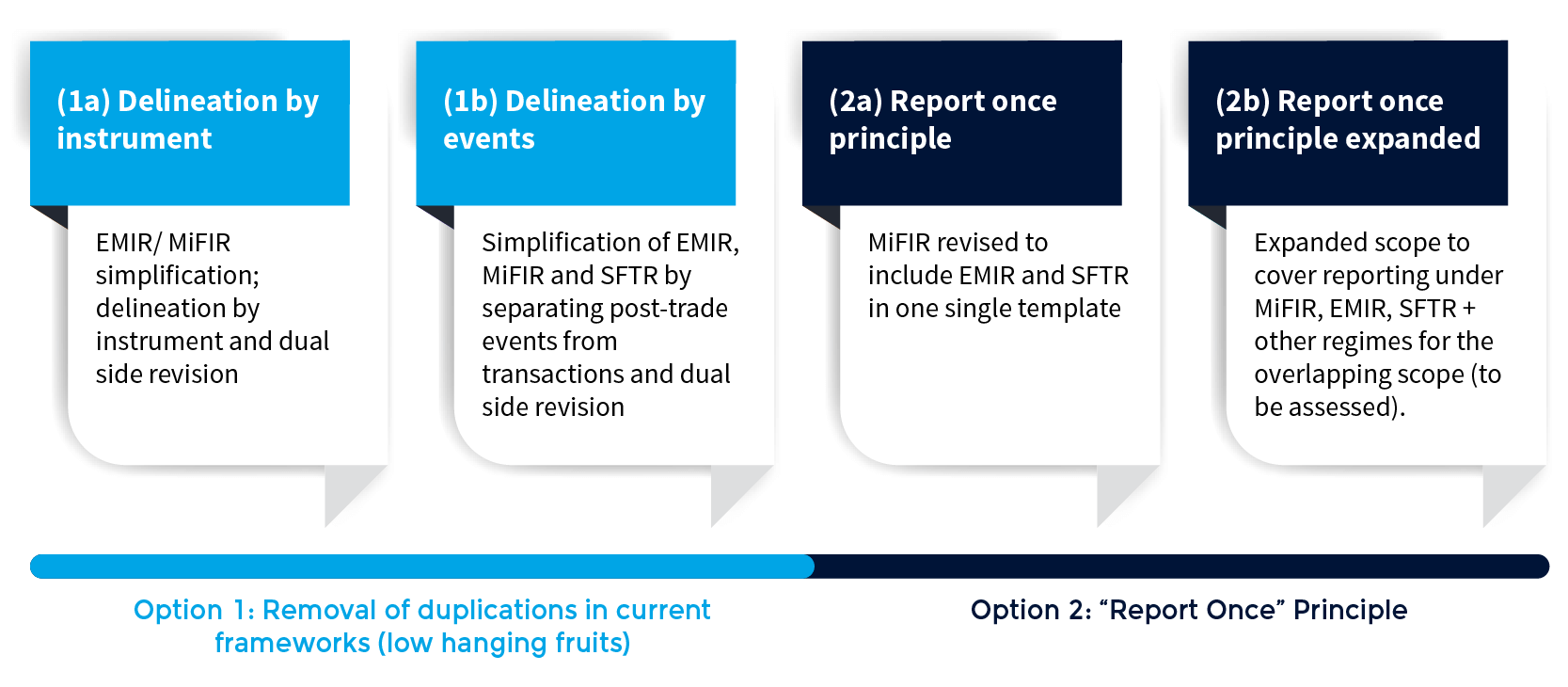

Option 1: Retain separate channels, with defined scope

The first option would keep the existing reporting channels but narrow their scope to reduce overlaps.

ESMA sketches out two possible approaches. One would split responsibilities by instrument type — EMIR for OTC derivatives, and MiFIR for exchange-traded ones. The other would divide them by event type, with MiFIR covering all transaction reports and EMIR focusing on post-trade updates.

In both cases, SFTR reporting could be folded into the revised frameworks to cut duplication and fragmentation further.

Option 2: A unified system

The second option is more radical, and would scrap the current patchwork of regimes altogether, introducing a unified “report-once” system instead.

This option also comes in two variations. One would apply a common template across MiFIR, EMIR, and SFTR, while the other would extend it to cover additional regimes, such as REMIT.

Both suboptions would also revisit EMIR’s dual-sided reporting model, which requires each side of a derivatives trade to report separately — a system prone to duplication and data mismatches.

In its Call for Evidence, ESMA sought respondents’ views on how far simplification should go and what trade-offs it might bring. They requested feedback on the cost, implementation risks, and transition challenges of each model. The Call for Evidence also explored whether new technologies — such as DLT and smart contracts — could help automate or even embed reporting directly within transaction systems.

While ESMA assesses feedback from the consultation, it has paused its broader MiFIR review to avoid overlap until the wider reform direction becomes clear. Planned updates to the reporting technical standards — RTS 22 (transaction reports), RTS 23 (reference data), and RTS 24 (order data) — are therefore on hold for now.

What’s next: ESMA’s final report and implementation timeline

With the consultation now closed, ESMA plans to publish its final report in early 2026, outlining key areas for simplification, and a preferred model based on stakeholder feedback. The report will then move through the EU’s legislative machinery before ESMA begins drafting the detailed technical standards.

Simplification won’t happen overnight. The implementation of both options could take five to seven years, with the “report-once” model expected to come later. So, the current MiFIR, EMIR, and SFTR regimes are likely to stay in place for a while.

Still, once the final report is out, firms should have a clearer view of ESMA’s direction — and a window to start preparing for what comes next. Industry discussions and working groups are expected to gather pace as the outlines of the new regime take shape.

Regardless of which simplification model wins, the message for firms seems clear: reporting will become more automated and data-driven. Those that invest early in smarter systems may be best placed to stay compliant — and ahead — as the regulations evolve.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.