Pricing credit risk with cutting-edge precision

Challenging conditions on financial and labor markets, affect both corporates and the banking sector, making the pricing of credit risk a priority. With Silicon Valley Bank’s sudden collapse and Credit Suisse’s unexpected takeover by UBS in background, market focus is back on credit risk assessment and pricing methodology.

The International Financial Reporting Standard 13 (IFRS 13) sets out the framework for measuring fair value and specifies that two forms of credit-related adjustments should be considered: a credit valuation adjustment (CVA) and a debit valuation adjustment (DVA) to reflect the counterparty’s or the entity’s own default risk. However, this Standard didn’t define the methodology further. The Institute of Public Auditors in Germany (IDW) later published the guideline HFA 47 with the recommended approach i.e. the advanced method.

This blog looks at two different approaches to pricing credit risk. Both use the same market data. However, the more sophisticated period-dependent approach allows for precise calculation of risk and fair value, thanks to using conditional probabilities of default that are tailored to every exposure period.

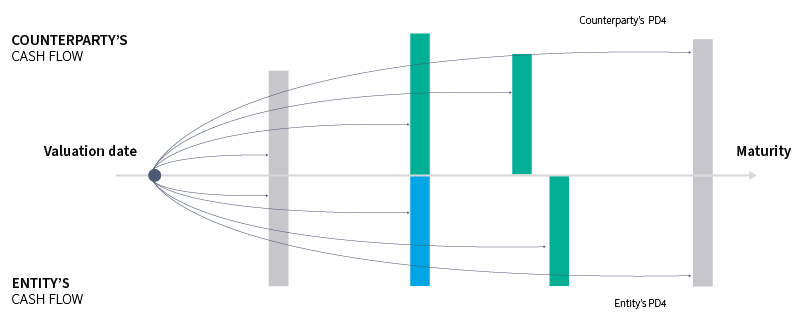

The previously used method: Expected Present Value

Under this method, probability of default (PD) curve based on CDS spreads and recovery rates is calculated. Every future cash flow is adjusted for credit risk using the entity’s own or the counterparty’s PDs. The sum of the cash flows’ risk adjustment equals the trade’s CVA/DVA.

This method uses accumulated PDs results in a probability of default curve that’s valid on the key valuation date and consists of predefined tenors. Each PD reflects the information available on the valuation date for a date in the future:

However, this calculation method doesn’t take into account one important piece of information: the future cash flows are going to be paid only if the party hasn’t defaulted in the period before that. The advanced method addresses this problem.

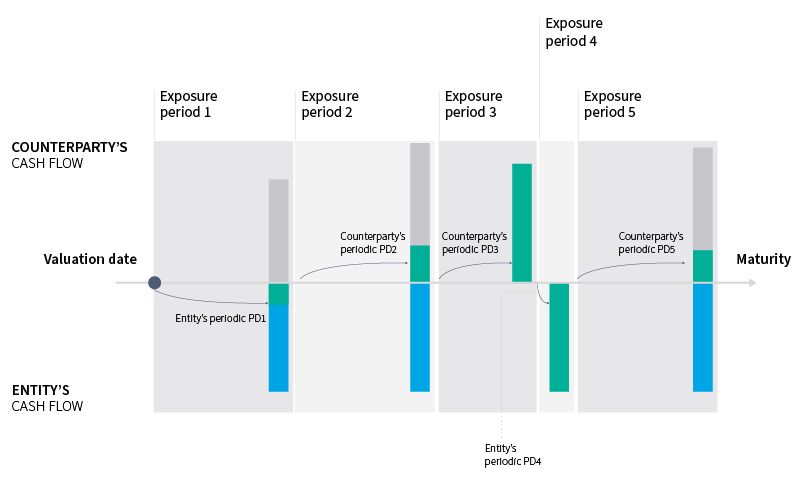

The advanced method: Period-Dependent Approach

This method uses the same market data as the Expected Present Value but with the period-dependent approach, financial instrument cash flows are divided into periods based on the maturity of each cash flow.

For every period, net exposure at default and periodic probability of default are calculated:

- Value dates of the cash flows define the period length.

- Net exposure is defined as a sum of discounted cash flows in the valuation’s currency.

- Periodic PD is calculated separately for the entity and the counterpart. It is conditional on not defaulting in the previous periods.

Based on the exposure sign the CVA or DVA is calculated for every exposure period. The sum of periodic risks shows the CVA/DVA for the whole trade.

ION Treasury recommends using the advanced method to comply with reporting requirements, as depending on the payment structure of the trade and the credit risk outlook, the valuation difference between the two approaches can be significant.

ITS, ION’s treasury management system supports above approaches highlighted above. ITS provides a comprehensive solution to the challenges of credit risk pricing, using cutting-edge technology and advanced methodologies recommended by auditors. With its ability to automate the pricing process and refine the pricing based on default risk changes, ITS is an asset for any organization looking to accurately price its credit risk.

Discover what ION can do for you

No matter where you are on your digital journey, ION Treasury has a solution that fits your needs. Contact us to learn more today.