Unlocking FX swaps: The migration to electronic channels gathers pace

NOTE: This article was originally published on e-Forex.net by Vivek Shankar.

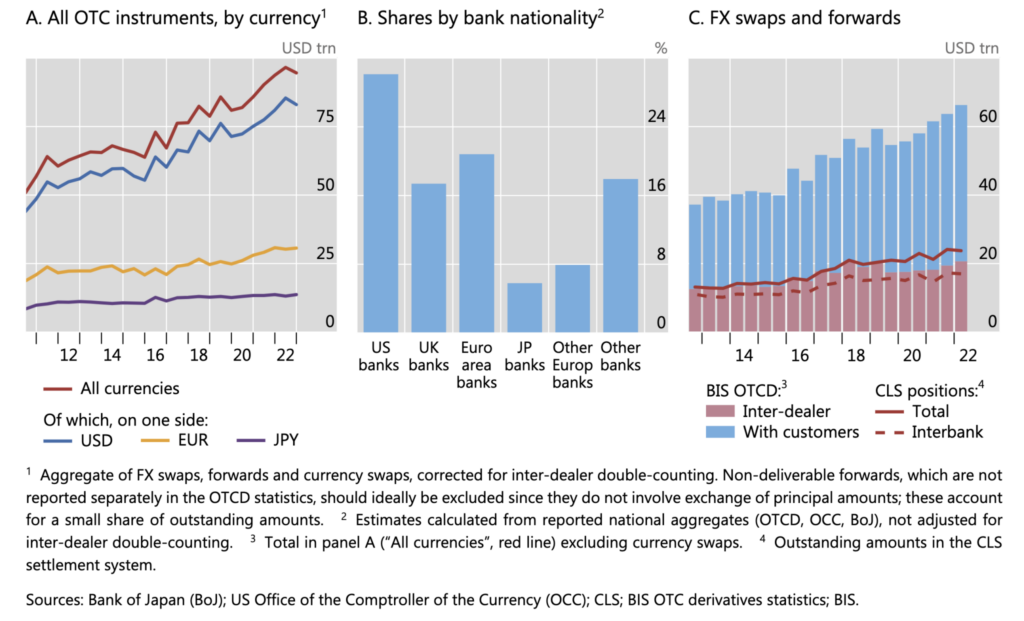

In 2023, the Bank of International Settlements reported that daily new FX swap contract volumes averaged $4 trillion. Undoubtedly, rising interest rates have played a part in increasing demand for Swaps. But what about other factors like higher capital charges for repos and money market instruments? Vivek Shankar investigates.

Brian Bunyan, Product Manager at Barracuda FX, part of the ION Markets (FX) product suite, says they have certainly played a role. “Banks are seeking ways to reduce the impact of capital charges imposed by the Basel capital framework,” he says. “Given the off-balance sheet nature of FX swaps, they present a more capital-efficient approach to funding for banks.”

The rising use of swaps as a capital-efficient funding option is encountering issues thanks to swap pricing complexities. While data is playing a role in simplifying this process, an increasing demand for swaps is revealing new challenges in this fascinating market.

Here’s why the FX swap market is growing and how technology service providers are helping firms overcome challenges along the way.

Swap demand drivers and dealing with pricing complexity

Bunyan says that technological innovation is another factor contributing to swap demand. “Increased electronification and automation has improved price quality, availability, and transparency across an expanded range of tenors/dates and currency pairs while also reducing the administrative burden of FX swaps activity and providing enhanced workflow efficiencies,” he says.

Meanwhile Jay Moore, CEO and Co-founder of FX HedgePool, feels passive trading strategies are playing a role. “Much of the FX swaps market is related to passive hedging of international exposures and/or global fund distribution strategies where cross border currency risk is often an unintended by-product of the investment itself,” he says. “The growth of these strategies, across both investment and investor geographies contributes to increased investment and the associated increased currency risk.”

“On the active side,” he continues, “global yield differentials create opportunity for active risk-taking both in terms of discretionary exposure to currency risk as well as active participation across the yield curve in terms of contract tenor.”

As demand builds, Phil Hermon, Executive Director, FX Growth & Execution at CME Group, says the FX swap electronification trails and this is creating pricing challenges. “FX swaps are trailing behind spot, forwards, and NDFs in terms of electronification and the potential benefits this can provide,” he says.

“Trading inefficiencies exist within the FX swaps market because the ecosystem is reliant on fragmented request for quote (RFQ) and request for stream (RFS) liquidity pools,” he continues, “in which clients need credit with a given liquidity provider to see or trade a given price.”

“This reduces transparency and certainty of execution, makes automated trading activity harder, and, ultimately, creates potentially worse trading outcomes for end users.”

While there is plenty of room to increase electronification in the swaps market, Peer Joost, CEO of DIGITEC, says that speed, scalability, and robustness are of particular need in any solution. He highlights the scale of the problem.

“As trading firms look to improve pricing, they are building ever more sophisticated pricing models which increasingly go beyond existing market data, to include yield curves and inferred FX swap points.”

“For a large Market-Making bank, up to 20,000 data points need to be priced along a forward curve, which quickly adjusts when the market starts to move,” he explains. “Models that solely rely on FX swap prices published by brokers are particularly vulnerable, as these data points are not only among the last to update in times of movement, they also do not cover relevant points such as central bank dates and liquidity events (such as month- and year-end) that show the largest effect.”

Bunyan notes that some portions of the pricing flow have benefited from automation. “At areas of the curve where the vast majority of trading is focussed (90% less than 3 months, 70% 1 week or less,)” he says, “the larger banks have already automated the majority of client pricing having deployed powerful pricing engines that provide enhanced yield curve modelling and FX swap price construction.”

“The focus more recently has been on solving issues to enhance automated risk management and inter-dealer market execution.” He notes that as electronification expands to risk management and interdealer market execution, clients will see the benefits of better quality pricing.

Moore feels this improvement is sorely needed. “The recurring and predictable nature of many hedging transactions put buy-side traders at a significant disadvantage when it comes to pricing,” he says. “Even when a trader can comp an order to several banks and accept what appears to be the best price, the predictable nature of the position may have allowed the banks to pre-hedge the order, which ultimately results in market impact.” He points out that most TCA measures do not capture these market impact costs since execution is compared to the market price at the time of execution, well after the impact has occurred.

Given the fragmented nature of the swaps market and its inherent challenges, how are technology providers introducing more automation?

Electronification in pricing and execution

It’s no secret that voice trading dominates swaps. Voice’s dominance is giving technology providers insights into the pain points they have to solve to introduce more electronification in the market.

Hermon points to the intertwined nature of credit and liquidity in OTC FX swaps. “Typically, both counterparties in a trade need an ISDA agreement and sufficient bilateral credit to proceed,” he says. “We aim to build liquidity on discrete points along the FX swaps curve within a central limit order book (CLOB), enabling algorithmic and API trading, while still providing options for manual trading through various front-end GUIs.”

This approach separates credit from liquidity, eliminating the need for documentation or a credit line between trading counterparts. “Introducing a CLOB with firm, no last-look pricing that operates 23 hours a day and is truly all-to-all can significantly enhance transparency and certainty for traders,” he says.

Moore notes the same challenge as Hermon and says, “FX HedgePool has developed fully integrated end-to-end workflow solutions to allow the buy-side to access liquidity from any number of counterparties, including peers, while adhering to account level broker restrictions and credit limits.”

“Having addressed the complex credit and allocations requirements of the buy-side, a much broader range of liquidity providers can now be accessed, creating less fragmentation and more efficiency.”

Stephan von Massenbach, Chief Revenue Officer at DIGITEC, says automation is increasing in pricing. “Workflows continue to be automated,” he says, “in price discovery and producing an accurate swaps price, as more market data from multiple sources is integrated with pricing engines. Our clients integrate the DIGITEC/360T Swaps Data Feed (SDF) to further improve accuracy and then use D3 to distribute prices to venues.”

von Massenbach says OMS is the next target for automation, enabling banks to place orders on interdealer Swaps venues. ION FX’s Bunyan agrees that electronification in interdealer execution has lagged.

“LSEG Forwards Matching and more recently 360T SUN have added APIs to allow users to trade electronically,” Bunyan says. “However, electronification of credit checking has been relatively slow for interdealer FX swaps.”

He says credit checks follow a manual process instead of using a “hard credit” check that is built into an electronic workflow. “We are seeing an increased focus on addressing this issue,” he continues. “360T SUN currently offers this capability (by maintaining limits in 360T or integration with a proprietary credit system), and LSEG Forward Matching is due to address it this year.

Efforts to improve the automation of credit for FX swaps will continue to be a focus.”

Data and technology delivery models

While the swaps market undoubtedly needs more pricing transparency, a swap’s structure creates a significant roadblock. “Market data and transparency around pricing are essential to an efficient market – from which FX swaps are a far cry,” Moore says.

“The bespoke nature of the swaps market makes it very difficult to find a like for like comparison of pricing. Unlike spot trading, it’s very difficult to identify comparable trade data in terms of size and tenor at the moment of the trade. “

He explains that the buy side currently relies on LP input for price reference points, considering those as “fair” values. Bunyan says the market is shifting away from this.

“The FX swap market’s shift away from pricing sources largely based around broker published FX swap points for a limited range of tenors to higher quality real-time streaming data feeds with granularity across the full curves has been a key enabler of electronification and automation,” he says.

Bunyan says these price feeds help users build fully automated real-time curves with greater accuracy and granularity. “We are also seeing greater availability of these feeds for currencies where data was particularly limited in the past thus enabling accurate full-curve automation for a wider range of currencies,” he adds.

“A key source of reliable FX swaps data is provided by the DIGITEC/360T Swaps Data Feed (SDF),” DIGITEC’s Joost adds, “which enables clients to build fully automated and accurate real-time curves. The SDF is based on participating major FX banks’ raw pricing, which represents Interbank quality.”

He also lists the STIR Futures Market as a good data source and says that pricing data of key instruments like the one and three-month USD SOFR Futures and the three-month EURIBOR

Futures need supplementing with market data from other assets, creating a cohesive pricing model.

“While the short end of the curve is based on Futures,” Joost continues, “the long end required to price Cross-Currency Swaps will need to be built out of Swaps. Here, the effect of the LIBOR transition can be observed.”

He notes that with LIBOR’s phasing out, the IRS market isn’t the source of liquidity it once was.

“Some markets, such as USD, liquidity has already moved to OIS, while others are transitioning (GBP) or lagging (EUR). This highlights the need to be able to quickly adjust the pricing models once the liquidity has shifted.”

While technology is enabling better data delivery channels, how is it helping smaller institutions access the market cost-effectively? Surely, massive datasets and faster execution should benefit these firms.

Hedgepool’s Moore says no. “Unlocking the FX swaps market is about solving for the underlying complexities of FX, which is credit and account level allocations,” he says. “The reason why more all-to-all trading and alternative liquidity venues haven’t been able to modernise swaps the same way as it has for spot is because a swap is essentially a credit instrument, which requires ISDA’s and expensive credit carve-outs.”

He explains that many banks offer swaps as part of a broad array of services, with low-margin swaps offset by value-added trading opportunities. Moore feels this situation has prevented progress for real money buy-side institutions.

“FX HedgePool has pioneered the novel credit intermediation model to enable all-to-all matching of FX swaps,” he says. “This model leverages existing bilateral ISDAs between buy- and sell-side firms to deploy idle credit availability for the booking and settlement of swap orders in return for fixed fees for balance sheet usage.”

The result is any party with a credit sponsor can participate while preventing information leakage and its attendant market impact.

von Massenbach and Bunyan point to the rise of SaaS pricing engines operating in the cloud as a game-changer, helping smaller firms move away from pricing swaps on Excel.

“In the past, many of these banks would have struggled to justify the cost of on-premises applications deployed and managed on their infrastructure,” Bunyan says. “In more recent times, the availability of these pricing engines as SaaS applications via the cloud has made the solutions more accessible.”

Interdealer market electronification and the future

“For FX swaps to automate further, there is a requirement for an efficient and increasingly more automated interdealer FX swaps market to help firms make markets to clients and efficiently risk manage their positions,” DIGITEC’s von Massenbach says.

“At DIGITEC we developed D3 OMS, to increase workflow automation and enable traders managing FX swaps risk to connect directly and efficiently place orders in these interdealer FX swaps venues. We expect the result to be increased volumes on electronic interbank matching platforms.”

Moore feels this electronification is just a first step. “Why stop there? Like with spot venues where any trader, buy- or sell-side with a settlement sponsor can participate in the liquidity, having an FX swap dark pool for all market participants will lead to further efficiency for all,” he says.

He notes that while credit-sponsored FX swap trades will be more explicitly expensive than direct interdealer trading, the implicit benefits of participating in the same pools of liquidity levels the playing field in terms of the investor outcomes.”

“A buy-side using an ISDA-based credit sponsor is economically similar to a hedge fund paying a prime broker to access valuable pools of liquidity,” he says. “Think of credit as the membership fee to access private liquidity pools. The fees are offset by the membership benefits, including anonymity and market impact.”

“With solutions like FX HedgePool, FX swaps dark pools are no longer a fantasy, but a growing reality with a broad community of buy- and sell-side participants.”

ION FX’s Bunyan sees algo adoption increasing in swaps, in line with the rest of the market, and shines a light on clearing. “The need for clearing is perhaps less pressing in the FX swaps market but remains an area of focus,” he says.

“We are likely to see further efforts to increase its adoption for a range of reasons including to reduce capital costs, mitigate risks, and obviate the requirement to address the many credit challenges by centralising it.”

“Automation of EFPs and increased cross product fungibility,” he continues, “between FX cash and futures is another area in which growth is likely to occur going forward.”

Whilst CME Group’s Hermon says liquidity centralisation holds plenty of promise. “We believe that a combination of FX Link (for spot starting FX swaps) and spreads of FX Futures (for FWD starting FX swaps) can help play a critical role within the evolution of FX swaps trading.”

Hermon says many clients are already using these products, with a 21% year-on-year increase in volumes of G5 spreads traded outside of the roll in Q4 2023.

“FX Link volumes were 90% higher in 2022 compared to 2021 and have been broadly stable at their new level,” he continues. “Both FX Link and spreads of futures enable automation, transparency, and the separation of liquidity from credit, but continued adoption and investment from clients, and in particular banks, will be critical to achieve a meaningful evolution.”

Overall, the FX swaps market should expect greater levels of transparency, thanks to the role technology is playing in bringing more relevant data and enhancing cost-effective access to the market.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.