Optimizing Cboe strategy allocations with linear programming

Key Takeaway

- The Cboe’s strategy-based margin framework requires traders to group option positions into few recognized strategies. This creates a massive combinatorial optimization problem to minimize the overall options margin requirements.

- Traditional greedy algorithms are fast, but they often settle for suboptimal groupings, locking up excessive amounts of margin.

- By reframing the problem using Linear Programming (LP), we can mathematically guarantee the most margin-efficient strategy allocation. This can potentially unlock significant liquidity.

1. The hidden complexity of margin calculation

In derivatives trading, clearinghouses mandate that traders post margin to safeguard against counterparty risk. Some exchanges use deterministic, portfolio-wide stress tests, such as CME SPAN to calculate a single margin figure. The Chicago Board Options Exchange (Cboe) utilizes multiple models, including a strategy-based margining framework.

Under the Cboe rules, a portfolio’s total margin is calculated by grouping its individual option contracts into specific, exchange-recognized strategies. For example, vertical spreads, butterflies, or condors. Because structured, multi-leg strategies inherently hedge against market movements, they are considered far less risky than standalone, naked positions, resulting in a significantly lower margin requirement.

The catch? The exchange does not automatically identify these strategies for you. It places the burden entirely on the participants to partition their individual option contracts into these recognized groupings.

2. The combinatorial explosion and the limits of greedy heuristics

Imagine a simple portfolio with three call options at different strikes, with the same expiry date and the same underlying with the price $101:

| Contract ID | Type | Strike | Quantity | Settlement | Expiry Date |

|---|---|---|---|---|---|

| C1 | Call | $95 | -1000 (Short) | $6.50 | 25/12/2026 |

| C2 | Call | $100 | 2000 (Long) | $2.50 | 25/12/2026 |

| C3 | Call | $105 | -1000 (Short) | $0.80 | 25/12/2026 |

An automated system must decide how to group these contracts. Depending on how the system organizes them, the capital you’re forced to lock up changes dramatically:

- Naive grouping (treating all as “naked”): The system sees short and long positions separately, ignoring the hedge.

Total margin: $33,600 [1].

- Suboptimal grouping (basic spreads): The system pairs half of the long contracts with the first short (C1-C2), and the other half with the second short (C2-C3).

Total margin: $9,000. - Optimal grouping (the butterfly): The system recognizes that all the contracts can be used to form highly efficient butterfly spread strategies (C1-C2-C3).

Total margin: $7,300.

When a portfolio scales to hundreds or thousands of different contracts, the number of potential strategy combinations explodes combinatorially.

Currently, many production environments rely on greedy algorithms to navigate this maze. Greedy algorithms make the best local choice at each step. They might quickly spot a highly efficient butterfly spread strategy and lock it in. But in doing so, they might consume a contract that was secretly the key to unlock an even larger portfolio-wide margin reduction. In short, greedy algorithms lack the foresight to find the global optimum.

3. Linear programming: The mathematical silver bullet

Traditional option margin calculators cannot account for combinatorial strategy grouping. To move beyond the limitations of greedy heuristics, we turned to Linear Programming (LP). However, the Cboe margin formulas are inherently non-linear, featuring max functions and discrete jumps that seem incompatible with linear models.

The breakthrough comes from a crucial shift in perspective: linearizing the problem.

Instead of asking an algorithm to calculate the complex margin on the fly, we split the process:

- Stage 1: We scan the portfolio’s contracts to generate a complete list of every type of valid strategy that could be formed. We are not allocating contracts yet; we are simply mapping out the possible alternatives.

- Stage 2: We calculate the exact Cboe margin requirement for one unit of each candidate strategy. These complex, non-linear margin rules are now fixed, known constants.

- Stage 3: We feed the strategies and their fixed unit margins into a Linear Program. Instead of blindly brute-forcing millions of quantity combinations, the LP solver uses advanced mathematical geometry to navigate the possibilities. It finds the exact quantity of each strategy to utilize so that every contract is perfectly accounted for, and the total margin is as small as possible.

By reframing the challenge as an allocation problem, we leverage robust mathematical solvers that deliver a guaranteed global optimum.

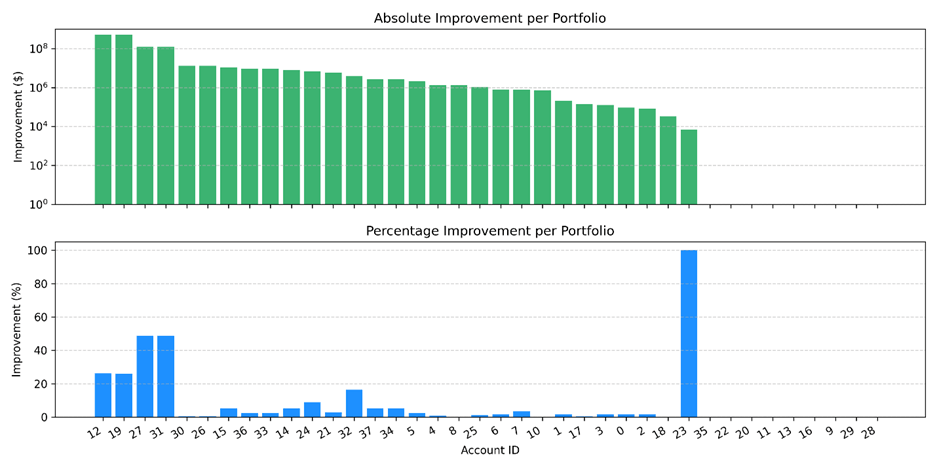

4. POC and results: Where optimization meets millions

We collected an empirical dataset of 38 actual, real-world portfolios, each comprising at least 10 different contracts. We then benchmarked our LP solution directly against a greedy algorithmic strategy.

Across the board, the globally optimal allocations found by the LP model outperformed the baseline. In the most complex portfolios, our LP formulation improved upon the greedy algorithm’s margin requirements by up to $500 million!

We mapped the performance across all 38 portfolios, generating histograms that plot the exact margin improvements. The distribution in these histograms highlights a consistent shift: the LP model extracts capital efficiencies that the greedy algorithm would waste. Each bar on that histogram represents millions of dollars in freed-up capital that could be deployed elsewhere, improving liquidity management and collateral allocation.

We mapped the performance across all 38 portfolios, generating histograms that plot the exact margin improvements. The distribution in these histograms highlights a consistent shift: the LP model extracts capital efficiencies that the greedy algorithm would waste. Each bar on that histogram represents millions of dollars in freed-up capital that could be deployed elsewhere, improving liquidity management and collateral allocation.

These results demonstrate that rigorous Integer Linear Programming has the potential to deliver maximum capital efficiency within Cboe portfolios.

[1] Margins computed using Cboe’s formulas.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.