New Scales of Change: Addressing the Challenges of Today’s Commodity Markets

Commodity markets are remarkably diverse. While financial commodities share many of the sales and trading characteristics of capital markets, physical commodities unlock a whole new realm of operational complexity and risk, write ION Commodities‘ Sunil Biswas, Chief Product Officer, and Richard Murphy, Market Owner – Liquid and Bulk Commodities. In this article, the authors explain the complexities and challenges that today’s commodities markets present to investment professionals.

The level of change and uncertainty across commodity markets worldwide is intense. Black swan events used to occur every few years. However, since COVID struck in 2020, we have seen black swan events and events of similar impact occurring multiple times per year.

From a commodities standpoint, consider oil prices and the shocks that these have generated most recently. The current price spike – produced by a ‘perfect storm’ of surging demand, overextended supply chains, unprecedented sanctions, and a shift to investing in renewables – has become a uniquely alarming issue.

Our crisis highlights that oil, unlike a typical capital market product – shaped primarily by the rhythms of interest rates and cash flow – is a complex physical commodity, with real-world intricacies in production, trade, storage, blending, and logistics. In an age of ongoing geopolitical volatility and exceedingly lean supply chains, every stage of an already precarious trading life cycle is exposed to great risk and so, extreme disruption.

Against this backdrop, the onset of a global energy transition is transforming the traditional suite of commodities to include renewable energy. This transition will influence our global system in ways that will profoundly affect our lives, businesses, and institutions.

The complex nature of physical commodities

Commodity markets are remarkably diverse. While financial commodities share many of the sales and trading characteristics of capital markets, physical commodities unlock a whole new realm of operational complexity and risk. Such complexity is largely caused by the need to move and blend physical commodities, which impact every aspect of the business, especially pricing and logistics.

To demonstrate this point, consider a moderately-sized crude marketer who wishes to get their products to the marketplace. They must manage purchases from producers at more than 2,000 leases. In addition to this, there is scheduling, tracking, settling, and invoicing for not only the 2,000+ lease purchases, but also the 10,000+ logistical movements to get the product to market. With this level of complexity, even the most basic profit and loss (P&L) report is a challenge.

New scales of disruption

While physical commodity markets are structurally complex, lean supply chains and extreme levels of asset optimization have magnified volatility.

In the interest of cutting costs and creating efficiencies, logistics companies and their customers have sought to make global supply chains as lean as possible. However, with less margin allowed for error, local disruptions have been exacerbated, even leaking into other geographies.

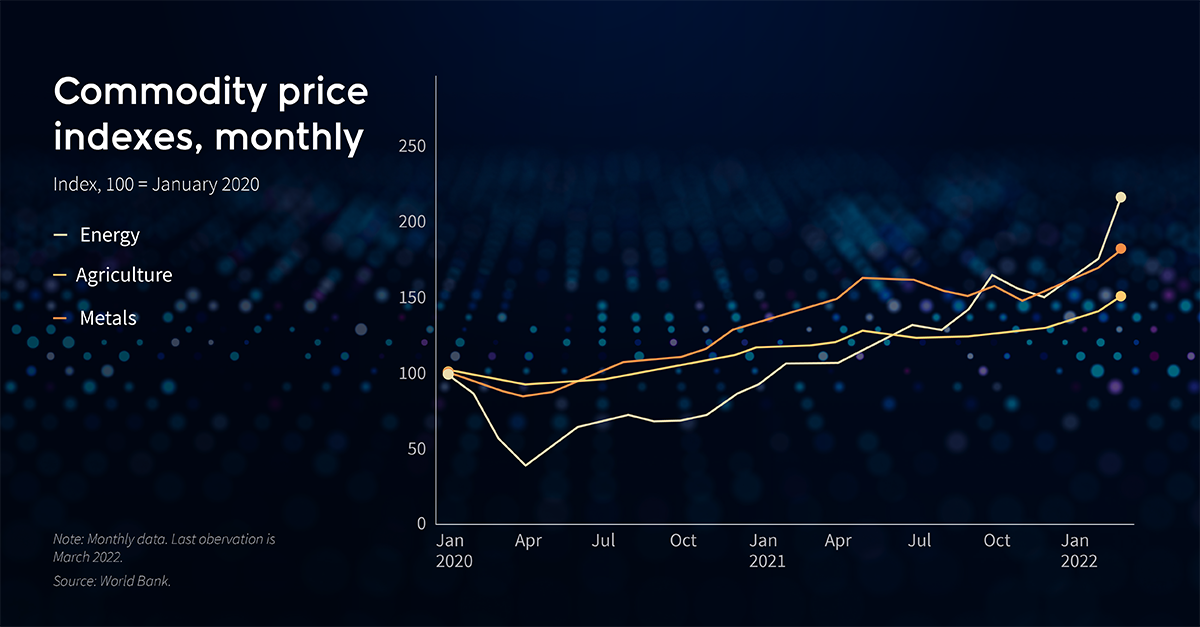

Just in one year that is, during 2021, we witnessed a range of disruptions: a global shortage in metals, such as copper, that are crucial for infrastructure; mass power outages in the ‘Texas Freeze’; extreme weather, forcing refineries and petrochemical plants to shut down; a major pipeline outage due to a ransomware attack, and the profound Suez Canal blockage of March 2021.

This year has already seen plenty more disruptions, such as Russia’s invasion of Ukraine and subsequent sanctions against Russia; and lockdowns across China due to a resurgence of COVID cases.

Combined with growing electric vehicle (EV), solar and wind mandates, these changes have caused lithium, carbon, nickel, copper, and rare earth metal prices to spike as the world’s mining industry faces increases of 300% to 1000% in demand over the next five to 10 years. So, many metal and mineral prices have doubled or tripled since 2020. In prior years, any one of these events would be incredibly rare. Now, their occurrence is regular – indeed, almost expected.

The structural challenges of the energy transition

Though we expect fossil fuels to remain our dominant energy sources until at least 2050, global ambitions to make a decisive switch to renewables will take several decades and impact every industry, especially commodity-intensive corporations.

Crucially, new renewable energy products and technologies are still maturing. Renewable energy used to comprise only solar- and wind-generated power and EV (battery powered) vehicles but now includes hydrogen, renewable fuels, and blends of fossil and renewable fuels.

Also included are the certificates associated with these renewable energy products. These additions have introduced new complexities across the value chain in dealing with the greatly expanded set of products and associated certificates impacting forecasting, trading, storage, blending, logistics, and consumption. Critically, carbon markets and certificates, relating to the transition, are often thinly traded.

Low volumes and increased volatility make pricing and risk all the more challenging, while new and unfamiliar counterparties across these classes introduce further uncertainty into every transaction.

Meanwhile, regulations and incentives around the energy transition have transformed established markets with a single piece of legislation or court ruling. Consider the sanctions put in place this year against Russia, one of the largest exporters of commodities worldwide. Gasoline, diesel, jet fuel, coal, gold, palladium, wheat, corn, and other products in every major commodity class reached an all-time high, or decade-high prices, from March through May.

It is hard to dispute the role of energy transition in driving many of the key challenges that commodity markets are required to balance and resolve. Power companies, accustomed to tracking and trading in power generated by fossil fuels, are these days required to track wind, solar, and other forms of ‘green’ energy, in parallel. Natural gas companies now manage hydrogen and LNG, while refined fuels companies are adding sustainable fuels, biofuel blends, and electric charging to their existing portfolios.

For these market players, supply and demand forecasting have become broader and more demanding, while logistics are becoming increasingly detailed and complex — demanding dedicated tanks, dedicated transportation assets as well as specialized settlement, invoicing, and accounting processes; all to ensure products are not co-mingled but are instead delivered to the correct locations in the correct quantities and on time. Above all, government-mandated environmental certificates and proof of sustainability documents must also be tracked across the value chain.

What lies ahead?

The global financial crisis of 2007-08 and aftermath accelerated the transformation of capital markets, driving significant structural changes. Today, we reckon on a similar tidal wave of change across commodities markets, which require effective standards and technology to weather modern challenges successfully.

For those who operate in these markets, having a clear understanding of risk, inventories, purchase and sale obligations, and logistical movement, is essential for optimizing business and improving profitability. Amid a global energy transition, scores of new products become impossible to manage without systems that automate the complicated processes behind them.

If one thing is clear, it is that today’s industry requires refined tools, real-time capability, and better standards to build resilience into commodities markets, where disruptions and vulnerabilities will continue to be felt universally.

NOTE: This article was originally published in TabbFORUM.