Cash management tools and techniques

As companies prioritize streamlined processes and fortified internal controls, the quest for sophisticated cash management solutions has intensified. This shift towards standardized and centralized activities underscores a growing recognition of cash as a multidimensional asset. Governmental initiatives aimed at harmonizing tax regulations and modernizing banking systems are reshaping business structures, impacting cash management frameworks. The global push for enhanced connectivity in banking and payments infrastructure is opening new avenues for innovation in cash management. The convergence of cash, liquidity, risk, and trade management is becoming more pronounced, expanding the scope of cash management beyond solvency and payment transactions. Accelerated by the global pandemic, investment in technology solutions has surged, leading to improved visibility and risk mitigation. Concurrently, the adoption of enterprise-wide processes and data standards is facilitating the emergence of integrated treasury functions aimed at achieving greater operational efficiency.

Cash pooling is a more streamlined way for companies to handle their funds and make financial operations. It includes combining cash from different accounts and legal entities to improve cash flow management and maximize interest returns. These are some types of cash pooling structures that exist:

- Physical cash pooling:

- Combines money from multiple accounts into one central master account.

- Can be done at the end of business or in real time.

- Helps minimize borrowing costs and increase interest earnings.

- Facilitates efficient use of funds, especially when one account has surplus funds and another has a deficit.

- Notional cash pooling:

- Funds remain in individual accounts without physical transfers.

- Balances in accounts are notionally offset against each other.

- Interest is calculated based on net balance.

- Useful for firms aiming for optimal returns on interest payments without moving funds physically.

- Multinational enterprises with branches in different countries often employ this method to combine finances and lower borrowing costs.

- Hybrid cash pooling:

- Combines elements of both physical and notional cash pooling.

- Allows companies to benefit from either system as needed.

- Maximizes interest income and reduces borrowing costs.

- Effective for companies with subsidiaries in different parts of the world, enabling effective fund consolidation while allowing physical transfers when necessary.

The right cash pooling structure selection relies on the individual needs and goals of a company. Understanding the differences among these forms of cash pooling helps businesses to better streamline financial operations, boost their money management capacities, and make informed decisions.

Benefits of cash pooling

Cash pooling is a valuable financial strategy that empowers companies to consolidate funds from various accounts into a single centralized account. This method offers numerous benefits, enhancing financial efficiency and providing a clearer overview of the company’s monetary resources. Let’s delve into the advantages of cash pooling and how it can be advantageous for businesses, regardless of their size.

Increased interest incomeBy consolidating funds into a single account with a higher interest rate, companies can maximize their interest income. This is particularly beneficial when dealing with multiple accounts across different banks, each offering varying interest rates.

| Benefits | Explanation |

| Reduced borrowing costs | Centralizing funds through cash pooling enables companies to offset short-term cash deficiencies from a centralized pool, reducing reliance on expensive short-term borrowing options like bank overdrafts and credit lines. |

| Improved cash flow management | Cash pooling provides a centralized view of funds, facilitating effective cash flow management. It helps in identifying surplus or deficit cash positions, enabling timely actions to ensure sufficient liquidity to meet obligations. |

| Simplified account management | Managing multiple accounts can be daunting. Cash pooling streamlines this process by offering a centralized overview of funds, reducing administrative burdens and providing a more accurate financial snapshot. |

Cash concentration explained

Cash concentration stands as a pivotal treasury management technique, aimed at consolidating cash from diverse accounts into a singular account to bolster cash visibility and control. Through centralizing its cash reserves, a company can efficiently manage liquidity, optimize cash flow, and mitigate the costs associated with banking services linked to maintaining numerous accounts.

How does cash concentration work?

Identifying cash balances:

- The process initiates with identifying cash balances dispersed across various bank accounts. This can either be done manually or through automated cash management systems, streamlining the aggregation of data from various sources.

- Automating cash management processes can alleviate the burden of dealing with a large volume of transactions, making the procedure more efficient and less prone to errors.

Consolidating cash balances:

- Following the identification of cash balances, they are consolidated into a solitary bank account. Various methods can be employed for consolidation, including wire transfers, automated clearing house (ACH) transfers, or physical transfers of cash or checks.

Reconciling transactions:

- Post-consolidation, transactions are reconciled to ensure alignment between the consolidated balance and the sum of individual account balances. This step is crucial in identifying and rectifying any discrepancies or errors in the cash concentration process.

Investing excess cash:

- Surplus cash, exceeding immediate needs, can be channeled into investments to generate returns. Options for investment range from short-term vehicles like money market funds to longer-term investments such as treasury bonds.

Managing cash flows:

- Cash concentration empowers companies to efficiently manage cash flows by centralizing cash balances. This heightened visibility into cash positions facilitates better forecasting of cash needs and more effective management of working capital.

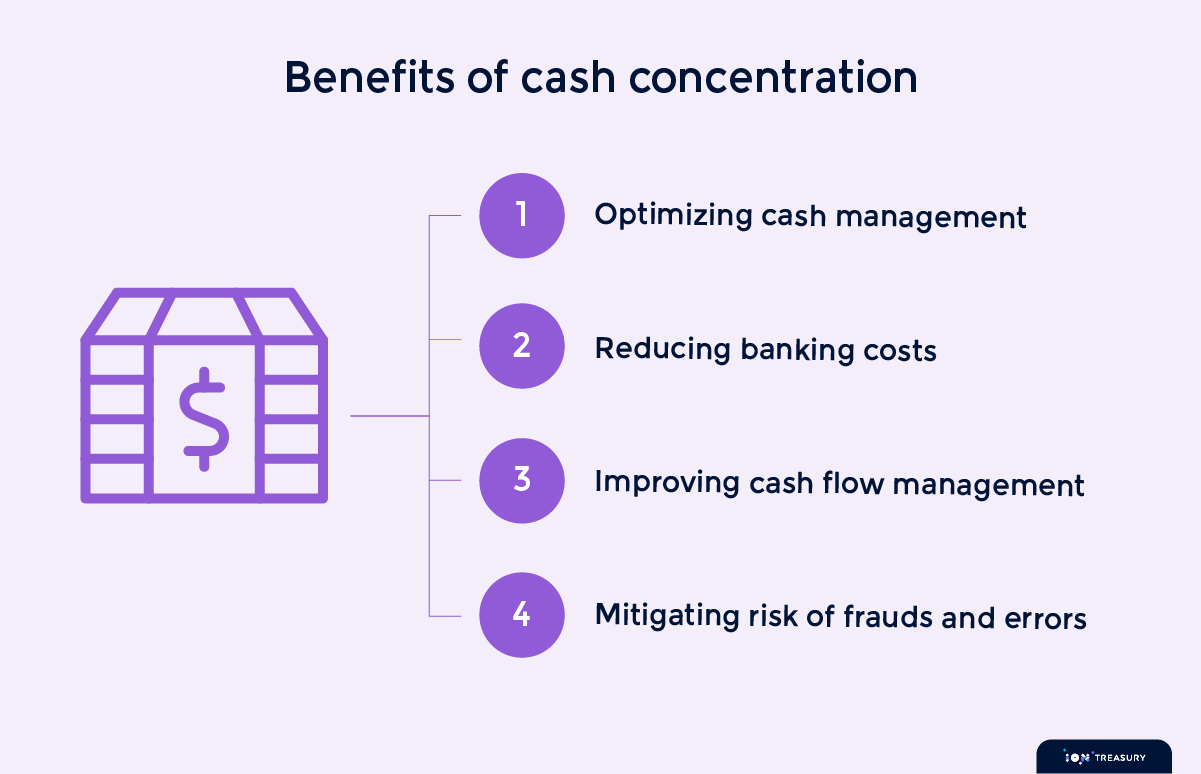

Benefits of cash concentration

- Optimizing cash management: Centralization enables companies to gain better insight into cash positions, aiding in effective cash management, forecasting cash needs, and optimizing working capital.

- Reducing banking costs: By consolidating cash balances into a single account, companies can diminish the number of bank accounts, subsequently reducing fees and transaction costs, resulting in long-term savings.

- Improving cash flow management: Centralized cash balances facilitate better management of incoming and outgoing cash flows, bolstering cash flow forecasting and working capital optimization.

- Mitigating risk of fraud and errors: Consolidation enables easier monitoring and detection of fraudulent activity or errors in cash balances, thus fortifying financial integrity and safeguarding against losses.

In essence, cash concentration serves as a cornerstone in treasury management, furnishing companies with enhanced control, visibility, and efficiency in managing their cash resources.

Implementing a successful cash pooling system

Cash pooling is a strategic endeavor for companies seeking to streamline cash management and optimize their target cash balance. This collaborative approach involves consolidating cash balances into a unified account, enhancing cash management efficiency. A successful cash pooling system can significantly impact a company’s financial performance by reducing borrowing costs, maximizing investment returns, and improving overall financial agility. Here’s a comprehensive guide on implementing a successful cash pooling system:

- Identify the objectives of cash pooling

- Clarify objectives: Define the reasons behind pooling cash, desired benefits, and risk mitigation strategies.

- Common objectives: Goals typically include reducing borrowing costs, optimizing investment returns, and enhancing cash management efficiency.

- Strategic Alignment: Ensure the cash pooling objectives align with broader organizational goals.

- Choose the right cash pooling structure

- Evaluate structures: Assess available options such as physical cash pooling, notional cash pooling, and hybrid cash pooling.

- Consider pros and cons: Each structure offers unique advantages and disadvantages, necessitating careful consideration.

- Tailor to needs: Select the structure that best aligns with the company’s objectives and operational requirements.

- Select the appropriate cash pooling bank

- Bank evaluation: Consider factors like reputation, expertise in cash pooling services, and associated fees.

- Supporting infrastructure: Ensure the chosen bank offers adequate support, including reporting and analysis tools.

- Compliance and regulations: Verify that the bank adheres to relevant regulatory standards and compliance requirements.

- Develop a cash pooling agreement

- Document terms: Formalize the cash pooling arrangement through a comprehensive agreement.

- Specify responsibilities: Clearly outline the obligations of each party involved in the cash pooling arrangement.

- Legal compliance: Ensure the agreement is legally binding and encompasses essential elements such as service fees and reporting obligations.

- Implement Cash Pooling Policies and Procedures

- Establish guidelines: Develop robust policies and procedures governing cash pooling activities.

- Cover key areas: Address aspects such as cash forecasting, allocation mechanisms, and risk management protocols.

- Regular review: Periodically assess and update policies and procedures to reflect changing business needs and regulatory requirements.

Implementing a successful cash pooling system demands meticulous planning and execution across various fronts. By aligning objectives, selecting appropriate structures and banking partners, formalizing agreements, and establishing robust policies, companies can effectively optimize their cash management practices, reduce borrowing costs, maximize investment returns, and fortify their overall financial resilience.

Understanding the purpose and benefits of zero balancing

Zero balancing is a strategic cash management technique designed to streamline cash concentration and disbursement processes. By consolidating funds from various accounts into a single concentration account, companies aim to enhance liquidity management and optimize cash flow. The primary objective of zero balancing is to eliminate idle cash, reduce borrowing costs, and capitalize on investment opportunities.

For treasurers, zero balancing offers numerous advantages. Firstly, it provides a comprehensive view of the company’s cash position, facilitating informed decision-making and accurate forecasting. Secondly, it minimizes the risk of overdrafts and associated fees by ensuring efficient fund allocation. Lastly, zero balancing improves working capital management by enabling surplus funds to be utilized for investments or debt reduction.

Evaluating different zero balancing techniques

Companies have various zero balancing techniques to choose from, each with its considerations and benefits. Let’s examine two common options:

- Physical zero balancing: This method involves physically transferring funds from subsidiary accounts to a concentration account. While offering transparency, it can be time-consuming and may incur transaction costs, especially for companies with dispersed subsidiaries.

- Notional zero balancing: Here, subsidiary account balances are notionally offset against each other, eliminating physical fund movements. Notional zero balancing, often facilitated through cash pooling, offers efficiency gains and cost savings but may entail legal and tax considerations, especially across borders.

Selecting the best zero balancing solution

Choosing the most suitable zero balancing technique hinges on factors like company size, complexity, and regulatory environment. Consider the following:

- Operational efficiency: Evaluate implementation ease, ongoing maintenance, and associated costs. For instance, physical zero balancing may require additional resources, while notional zero balancing relies on robust cash pooling arrangements.

- Regulatory and legal considerations: Assess legal and tax implications, particularly in multi-jurisdictional operations. Seek guidance from legal and tax experts to ensure compliance.

- Technology and integration: Ensure existing systems support the chosen technique for seamless integration with treasury and accounting systems.

- Risk management: Evaluate each technique’s impact on liquidity, counterparty, and operational risks. Assess control and transparency levels to manage risks effectively.

Mastering cash management tools and techniques such as cash pooling, cash concentration, and zero balancing can significantly enhance a company’s financial agility and resilience. By centralizing funds, optimizing cash flows, and minimizing borrowing costs, businesses can unlock greater efficiency, mitigate risks, and capitalize on investment opportunities. With careful planning, diligent execution, and a commitment to continuous improvement, companies can navigate the complexities of cash management successfully, positioning themselves for sustainable growth and success in today’s dynamic business landscape.

Comparison of cash pooling, cash concentration, and zero balancing: features, benefits, and use cases

| Feature | Cash pooling | Cash concentration | Zero balancing |

| Definition | Combines funds across accounts into a centralized system. | Consolidates cash physically into a single account. | Consolidates funds from subsidiary accounts to a master account daily or periodically. |

| Structure | Notional (no physical transfer) or physical (actual transfer). | Physical transfer of funds from individual accounts to a central account. | Physical transfer of funds from accounts to a zero balance at the end of the day or a specific period. |

| Cash transfer | Optional in notional pooling, mandatory in physical pooling. | Mandatory physical transfer. | Physical transfer to zero balance. |

| Interest calculation | Notional pooling uses a net balance for interest calculation; physical pooling uses actual funds. | Based on consolidated central account balance. | Based on the single central account balance. |

| Control and visibility | Medium (depends on pooling type and system integration). | High, as all funds are consolidated in a single account. | High, as funds are centralized, ensuring complete visibility. |

| Implementation complexity | Medium; requires agreement on pooling structure and system integration. | High; involves account consolidation and often system upgrades. | Medium; requires coordination among accounts but less complex than concentration. |

| Regulatory constraints | Low for notional pooling; may vary for physical pooling (cross-border transfers). | May encounter regulatory hurdles, especially for cross-border accounts. | Few; typically simpler in domestic environments but may face cross-border tax considerations. |

| Cost | Lower for notional; higher for physical pooling (transfer costs). | Medium to high, depending on the volume of transactions and transfer fees. | Lower than concentration but higher than notional pooling. |

| Technological requirement | Requires compatible treasury systems for automation. | Requires advanced treasury and ERP systems for integration. | Requires treasury tools capable of daily reconciliation. |

| When to Choose | Use for flexible fund utilization across accounts or entities while retaining individual account operations. | Choose when centralized visibility and control over cash is needed, especially for investment opportunities. | Ideal for centralized disbursement and avoiding idle balances or overdrafts. |

Machine learning in cashflow forecasting

The integrity of cash flow management hinges on precision and foresight. According to an IBM report, a staggering 88% of spreadsheets harbor errors, jeopardizing the accuracy of financial projections. Flawed data leads to flawed forecasts, posing significant challenges for businesses striving to navigate cash flow dynamics with confidence and agility. However, amidst this uncertainty, the emergence of machine learning (ML), offers insights and predictive capabilities to fortify cash flow management strategies. Here are some key aspects highlighting the significance of ML in cash flow management:

Forecasting accuracy: ML algorithms can analyze historical cash flow data and identify patterns, trends, and seasonality factors that impact cash flow. By leveraging advanced forecasting models such as AutoRegressive Integrated Moving Average (ARIMA) or Long Short-Term Memory (LSTM), businesses can generate more accurate predictions of future cash flows. This allows organizations to anticipate cash shortfalls or surpluses and take proactive measures to manage liquidity effectively.

Risk management: ML algorithms can assess various risk factors affecting cash flow, including market volatility, economic conditions, customer payment behavior, and supply chain disruptions. By analyzing a wide range of data sources in real-time, ML-powered risk management systems can identify potential threats to cash flow and suggest mitigation strategies to minimize financial losses.

Credit scoring and collections: ML techniques are employed in credit scoring models to evaluate the creditworthiness of customers and determine the likelihood of timely payment. By analyzing customer transaction history, payment patterns, and other relevant data, ML algorithms can assign risk scores to individual customers and tailor credit terms accordingly. Additionally, ML-powered collections systems can prioritize delinquent accounts based on their probability of repayment, optimize collection strategies, and reduce bad debt write-offs.

Working capital optimization: ML algorithms can optimize working capital management by dynamically adjusting inventory levels, accounts receivable/payable terms, and cash conversion cycles. By analyzing historical transaction data and external market indicators, ML-powered working capital management systems can identify opportunities to reduce excess inventory, expedite receivables, and extend payables strategically, thereby freeing up cash for operational needs.

Fraud detection and prevention: ML techniques are instrumental in detecting and preventing fraudulent activities that can impact cash flow, such as payment fraud, invoice manipulation, or identity theft. By analyzing vast amounts of transactional data in real-time, ML-powered fraud detection systems can identify anomalous patterns or suspicious behaviors indicative of fraudulent activity and trigger alerts for further investigation.

Optimized investment decisions: ML algorithms can assist treasury departments in making informed investment decisions to maximize returns on excess cash reserves. By analyzing historical market data, interest rates, and economic indicators, ML-powered investment models can identify optimal investment opportunities while considering liquidity requirements and risk tolerance levels.

Power of sweep funds in cash flow management

Sweep funds, also known as cash sweep accounts, are financial instruments used by companies to optimize short-term investments and enhance cash flow management strategies. These accounts automatically “sweep” excess cash from checking or operating accounts into higher-yielding investment vehicles, typically money market funds or other short-term investment options. Here’s how companies leverage sweep funds to maximize returns on idle cash while maintaining liquidity:

- Liquidity management: Sweep funds offer companies a convenient way to maintain optimal liquidity levels by automatically transferring excess cash from checking accounts into interest-bearing investments. This ensures that funds are readily available to cover operational expenses, yet not sitting idle, earning minimal interest.

- Yield enhancement: By investing in money market funds or other short-term instruments, companies can earn higher yields on their idle cash compared to traditional checking or savings accounts. Sweep funds allocate cash to investments with relatively low risk and competitive returns, allowing companies to maximize earnings on their short-term reserves.

- Cash flow optimization: Sweep accounts help companies optimize cash flow by reallocating surplus funds to investment vehicles that offer higher returns without sacrificing liquidity. This ensures that cash reserves are deployed efficiently, earning incremental returns while remaining accessible for working capital needs or unforeseen expenses.

- Risk mitigation: While seeking higher yields, companies prioritize safety and liquidity when selecting sweep fund options. Money market funds, for example, invest in short-term, high-quality securities such as Treasury bills and commercial paper, minimizing credit and market risk. This prudent approach helps companies preserve capital while generating incremental income.

- Automation and efficiency: Sweep funds streamline cash management processes by automating the movement of funds between accounts based on predetermined thresholds or rules. This eliminates the need for manual intervention and ensures that excess cash is promptly invested or utilized for debt reduction, thereby enhancing operational efficiency.

- Regulatory compliance: Companies must comply with regulatory requirements governing the investment of corporate funds, such as restrictions on permissible investments and liquidity ratios. Sweep funds offer a compliant mechanism for investing excess cash in accordance with regulatory guidelines, thereby minimizing compliance risk.

ION’s treasury systems and Goldman Sachs’ Mosaic integration

To simplify sweep account management and enhance its efficiency, the integration between ION’s seven treasury management systems and Goldman Sachs’ investment portal, Mosaic, stands as an advancement in cash management solutions. This collaborative effort streamlines the utilization of sweep accounts, elevating their effectiveness in optimizing short-term investments for businesses. By integrating with Mosaic, these treasury management systems can:

- Streamline sweep account utilization, enhancing effectiveness in optimizing short-term investments for businesses.

- Automate the process of sweeping excess cash into money market funds with unparalleled efficiency through seamless integration with Mosaic.

- Provide real-time consolidated investment and cash reporting, facilitating more informed decision-making regarding cash positions.

- Give access to a comprehensive suite of money market fund data and analytics, enabling strategic fund allocation to maximize returns while preserving liquidity.

- Represent a transformative leap forward in cash flow management, offering unmatched convenience, efficiency, and financial insight for businesses of all sizes.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.