Using a local volatility model for the evaluation of TARF FX options

Key Takeaways

- TARF complexities require a non-standard pricing approach

- The Dupire model deals well with non-constant volatility cases

- This model plus a Monte Carlo simulation can price all TARFs

We wrote last week that Target Redemption Forwards (or TARFs) have many benefits but come with a downside risk as investors remain fully exposed to adverse exchange rate fluctuations.

This week we will run some numbers and discuss how these complex financial instruments used in foreign exchange (FX) markets require an evaluation approach that encompasses non-constant volatility inputs. TARFs, in fact, possess path-dependent features for which the standard Black-Scholes model with constant volatility is ill-suited.

The Dupire local volatility model

The first volatility smile (that is, a strike pattern exhibited by market volatility) was first seen in 1987 following the stock market crash. Since then, equity index option markets have displayed a dependency of implied volatilities on the strike price as well as on the time to maturity. These anomalous patterns appeared, therefore, in clear contradiction with the assumption of a completely flat volatility curve of the standard Black-Scholes option theory. This has led quants to address the limitations of this model and better capture the complex dynamics of the market observed in empirical data.

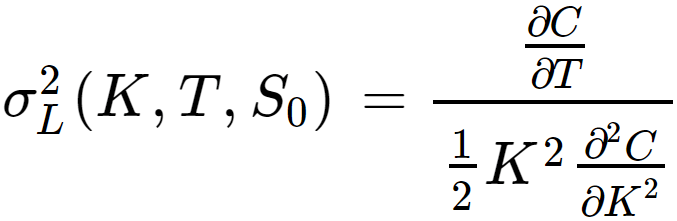

More sophisticated frameworks have been developed, including the local volatility approach proposed by Dupire, which was formulated as an extension of the Black-Scholes model and allows volatility to vary with the underlying asset price and over time. Within the Dupire local volatility model, the underlying spot S can be modeled through a stochastic process of the type:

where, as you can see, the volatility σ is a deterministic function of time and spot price. Dupire derived an equation that enables us to deduce the volatility function from quoted put and call options in the market, which reads as follows:

where C is the undiscounted option price of the option, K is the strike price, T is the time to maturity and S₀ is the initial asset price.

Given its formulation, the local volatility model is well adapted for pricing and hedging exotic options and other derivatives that are sensitive to the path of the underlying asset price, as TARFs are.

A Monte Carlo simulation

The Monte Carlo (MC) simulation is a useful technique for the evaluation of options with path-dependent payoffs. The model returns the price of an option as its discounted expected value. In our work, given the knock-out feature of TARFs, we have adapted the general procedure to the following steps:

- Generate a possible but random price for the first fixing date.

- Calculate the associated payoff of the option for the first fixing date.

- Compare the payoff with target (cap) level.

- If the payoff is greater than or equal to the target level, calculate the present value of the target level and the option is knocked out. If the payoff is less than the target level, calculate the present value of the payoff and go to the next fixing date.

- Repeat the above steps until the option expires or target level is reached to get the price pᵢ of the TARF on the ith path.

- Repeat the above steps N times.

- Calculate the average of the N generated prices pᵢ to get the final TARF price.

The Greeks

The Greeks are a set of financial indicators used to measure the sensitivity of an option’s price to different factors. In our MC simulation, we calculate them using a method called likelihood ratio (LR), explained in this 1996 paper by Broadie & Glasserman. This technique focuses on how the underlying probability density depends on the parameter we are interested in, rather than the option price itself. To compute a particular Greek, we take the logarithmic derivative of the probability distribution that predicts future values of the underlying assets with respect to the evolution parameters. Then, we weigh the value of the payoff function with the LR corresponding to the desired sensitivity for each simulated path and take the MC average.

Initializing the Dupire local volatility

To effectively use the Dupire formula for local volatility, we must accurately retrieve the market quotations and construct a sufficiently dense grid of implied volatilities across time-to-expiries and strikes.

Since we are mostly interested in pricing TARF-style FX options, we use a volatility matrix from the FX options market, which is built according to the sticky Delta rule. Under this rule, the options are priced depending on their Delta, so when the underlying asset price moves and the Delta of an option changes accordingly, a different implied volatility must be plugged into the pricing formula. Below, we show an example of an FX market quote volatility matrix for the EUR-USD exchange rate.

| Expiry | ATM | Δ 10 Butterfly | Δ 10 Risk Reversal | Δ 25 Butterfly | Δ 25 Risk Reversal |

| 1W | 0.0625 | 0.003925 | -0.0127 | 0.00115 | -0.00652 |

| 1M | 0.0655 | 0.003725 | -0.01287 | 0.001175 | -0.0067 |

| 2M | 0.0655 | 0.0047 | -0.01357 | 0.00143 | -0.00707 |

| 3M | 0.06375 | 0.00543 | -0.01447 | 0.00158 | -0.00728 |

| 6M | 0.0645 | 0.00662 | -0.0172 | 0.001875 | -0.00873 |

| 9M | 0.067375 | 0.00815 | -0.01955 | 0.0023 | -0.0098 |

| 1Y | 0.0673 | 0.01 | -0.0208 | 0.00275 | -0.01038 |

| 2Y | 0.0693 | 0.010475 | -0.02 | 0.00293 | -0.01015 |

| 3Y | 0.071975 | 0.0107 | -0.0186 | 0.0029 | -0.0094 |

| 5Y | 0.075325 | 0.0111 | -0.0164 | 0.0031 | -0.0083 |

| 7Y | 0.0818 | 0.0108 | -0.011 | 0.003 | -0.0062 |

| 10Y | 0.08525 | 0.011 | -0.0072 | 0.003 | -0.004 |

ATM refers to the at-the-money volatility. Risk Reversal is the difference between the implied volatilities related to buying a call and selling a put with symmetric Delta. Butterfly is the difference between the implied volatilities associated with selling an ATM straddle and buying a delta strangle.

By solving a linear system, we find the two implied volatilities (call and put) for the corresponding Delta value. Then, as we need to construct an expiry/strike grid, for each expiry we first determine the strike associated with each Delta (following some market convention) and then the new strike-volatility pairs (employing a specific interpolation method). Finally, after enhancing the granularity of expiry data to intervals as short as one day, we can create an N x M grid, where N and M are adjusted according to the evaluation performance we want to reach.

A calculation example

Here, we present a calculation example of a vanilla TARF payoff.

A vanilla TARF is a financial instrument with a cashflow (F – Sᵢ) x Neur, where F is a fixed exchange rate called Forward (EUR/USD in our example), Sᵢ is the exchange rate relative to the ith settlement date, and Neur is a fixed EUR amount. This transaction includes clauses for early termination; in fact, if on a specific date the total observed value (i.e. the sum of cashflows up to the current settlement date, sum_obs_qty) reaches or exceeds a certain threshold, T, that date becomes the Final Settlement Date, and the relative cashflow reads T – sum_obs_qtyt-1. After the Final Settlement Date, the transaction terminates and no further payments are needed. If you are interested in more details on the payoff specification you can look at this document.

The following two tables show the input data and the pricing results (including the Greeks) for the TARF instrument, while below a single Monte Carlo Scenario is shown with the corresponding USD cashflows for each instrument’s settlement date.

| Trade Date | 11-Sep-2011 |

| Forward | 1.46 |

| Spot | 1.390414 |

| EUR Amount | 100000 |

| USD Amount | 146000 |

| Target (USD) | 50000 |

| MC num. of paths | 65536 |

| value (USD) | error (USD) | |

| Price | 49388.4275 | 17.80719638 |

| Delta | -60390.0632 | 30107.56647 |

| Gamma | -4451207.93 | 9273095.125 |

| Rho | -13376.0212 | 509.1261979 |

| Vega | -47602.6439 | 13747.07912 |

| Theta | -11855.917 | 13178.0919 |

| Fixing Date/ Settlement Date |

Fixing Exchange Rate | sum_obs_qty | Cashflow (USD) |

| 9/28/2011 9/30/2011 |

1.249041679 | 21095.83211 | 21095.83211 |

| 9/29/2011 10/3/2011 |

1.253282678 | 41767.56435 | 20671.73225 |

| 9/30/2011 10/4/2011 |

1.250920584 | 62675.50593 | 8232.435645 |

| 10/3/2011 10/5/2011 |

1.239105371 | 84764.96886 | 0 |

| 10/4/2011 10/6/2011 |

1.230769021 | 107688.0668 | 0 |

| 10/5/2011 10/7/2011 |

1.203547523 | 133333.3145 | 0 |

| 10/6/2011 10/11/2011 |

1.195922513 | 159741.0632 | 0 |

| 10/7/2011 10/12/2011 |

1.176056375 | 188135.4257 | 0 |

Addressing TARF complexities

As we have seen, the complex and path-dependent structure of TARF instruments calls for a non-standard framework for their evaluation, where the local volatility model of Dupire comes in. Here we have demonstrated how, through this approach combined with a Monte Carlo simulation, we can price a TARF payoff, that of the simplest case, the vanilla one. However, this method is suitable to ideally price all TARF variants that, being different from each other, demand specific pricing models tailored to them.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.