Derivatives innovation: RTX and D2D execution automation

This content was originally published by Clarus.

This blog looks at RTX Fintech & Research (RTX), a recent start-up interest rate swap SEF (Swap Execution Facility).

Key Takeaways

- Despite the post-2008 regulatory nudge towards electronic trading protocols, most dealer-to-dealer (D2D) platform volume still uses the voice-brokerage trading protocols of the platforms registered as SEFs by the pre-existing IDBs.

- In September 2023, RTX launched a SEF which executes individual trades more electronically, aiming to simplify, automate, speed up, and reduce the cost of D2D trade execution.

- RTX reached a 5.1 percent share of D2D platform cleared Secured Overnight Financing Rate (SOFR) swaps risk-trading in December 2025.

Read on for more details.

All the charts, data, and statistics in this blog were sourced from SDRView.

D2D SEF development

After the 2008 Global Financial Crisis (GFC), the G20 consensus and national regulators exerted pressure to move swaps trading from bilateral voice-trading to clearing at CCPs and trading on multilateral electronic trading platforms (known as SEFs in the US and OTFs or MTFs in Europe).

In the early years after 2008, a market-wide initiative worked on the RFQ electronic protocol for SEF trading on dealer-to-client (D2C) platforms. For D2D platforms, the Central Limit Order Book (CLOB) model used by cash and futures exchanges was the most-discussed model for electronification, with start-up CLOB SEFs appearing alongside the SEFs registered by interdealer brokers (IDBs) for their established voice-brokerage businesses.

Since then, RFQ has become the dominant protocol for US D2C SEFs, while D2D CLOB SEFs did not sustain material market share away from the IDBs’ voice-brokerage SEFs. Dealerweb has successfully shifted to a session-based approach, while other CLOBs have closed. Nonetheless, the bulk of D2D platform activity today remains on the voice-brokerage platforms of the IDBs.

Note on volume metrics

For the rest of this blog, we look at USD Overnight Index Swaps (OIS) referencing the Secured Overnight Financing Rate (SOFR swaps) as this product is RTX’s current focus.

As our volume metric, we use the execution event count of SOFR swap risk-trading (package-adjusted USD OIS trade count excluding FedFunds OIS, compressions, and uncleared trades). We take this metric from SDRView, which allows us to filter out the noted exclusions and avoid the distortions of trade caps in the SDR reporting.

SDRView excludes trades not reported to US swap data repositories (SDRs) because they have no US participant, while SEFView shows complete SEF volumes but does not allow the specific execution event count with the filtering above. We compared the two services’ calculated market shares and trends on like metrics (notional/DV01) and on like product scope (all USD OIS including FedFunds, compression and uncleared). The resulting market shares and trends were not materially different.

Caveat: given this blog is based on trade volumes, it may not bring to light electronification initiatives within platforms other than RTX.

D2D volumes context

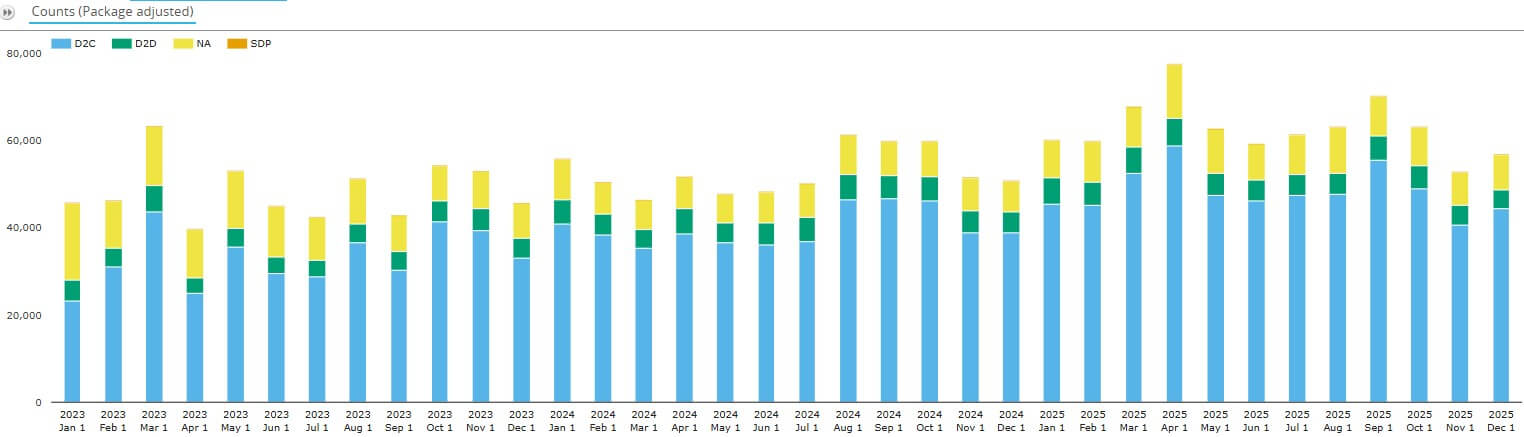

We start with month-by-month SOFR swap package count.

Chart 1: SDR-reported cleared SOFR swap risk-trading volumes by platform type (execution event count excluding compression). Source: SDRView.

The data in Chart 1 allows us to calculate and compare 2025 and 2023 average monthly execution events for SOFR swaps risk-trading. These totaled 39,100 in 2025 – up 37 percent from 28,500 in 2023.

- D2C platforms had 28,300 execution events per month in 2025 – up 50 percent from 18,900 in 2023.

- D2D platforms saw 5,100 execution events per month in 2025 – up 14.5 percent from 4,450 in 2023.

- Off-platform (NA) had 5,690 execution events per month in 2025 – up 11.3 percent from 5,110 in 2023. (Note: an off-platform trade may be either D2C or D2D).

Over the period, SOFR swap risk trading shifted onto platforms and D2C platforms grew faster than D2D platforms, perhaps because of greater automation.

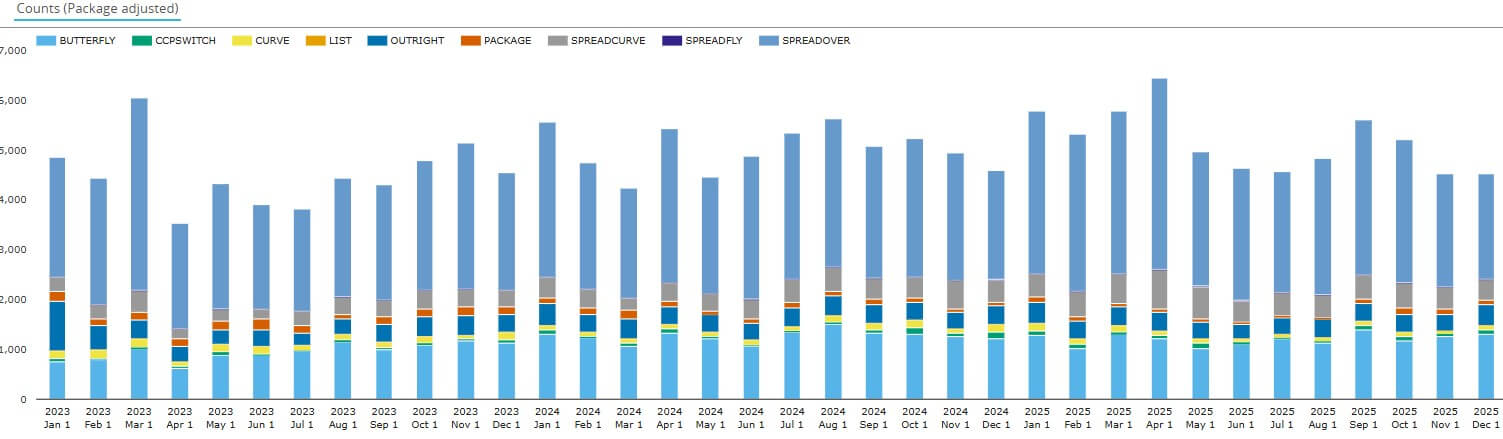

Now we look at D2D volumes in more detail. Here we exclude compressions to focus on risk trading package types only.

Chart 2: SDR-reported cleared D2D platform SOFR swaps risk-trading volumes by package type (execution event count excluding compression). Source: SDRView

Chart 2 allows us to break out the D2D monthly averages from Chart 1 by package type.

- Spreadovers averaged 2,870 SOFR swaps risk-trading execution events per month in 2025 – up 14 percent from 2,520 in 2023.

- Butterflies averaged 1,200 execution events per month – up 26 percent from 952 in 2023.

- Curve spreads (SPREADCURVE) averaged 519 execution events per month – up 70 percent from 306 in 2023.

- Outrights averaged 277 execution events per month – down 21 percent from 349 in 2023.

- Remaining packages in aggregate averaged 229 execution events per month – down 30 percent from 329 in 2023.

Enter RTX

RTX is led by:

- CEO James Cawley, formerly CEO of Javelin, a swap-trading CLOB SEF.

- Head of Markets Christopher Jonns, a long-time swap broker from TP ICAP.

I’m grateful to RTX for spending the time to explain further the details shown on their website.

RTX takes as a premise that pure CLOB is not a suitable electronic trading protocol for D2D swap trading platforms. Instead, RTX looks to automate the IDB voice protocol using its Request For Trade (RFT) protocol. RFT works by allowing market makers to enter firm bids and offers directly to the RTX screen, where any RTX participant can click to execute a bid or offer at the posted price on a first-come, first-served basis, without the possibility of withdrawal of the bid or offer.

Automated execution means that trades appear immediately in both parties’ risk systems and are more rapidly matched and sent downstream. Downstream means both parties’ back offices, RTX compliance, the DTCC SDR, and CME or LCH. The trade becomes certain to both parties sooner after the execution click, because a voice brokerage platform requires the broker’s trade support team to manually enter the matched trade before sending it to both dealers.

The result is to eliminate human steps, improve trading certainty, speed up trade execution and trade flows, and lower execution costs and brokerage fees.

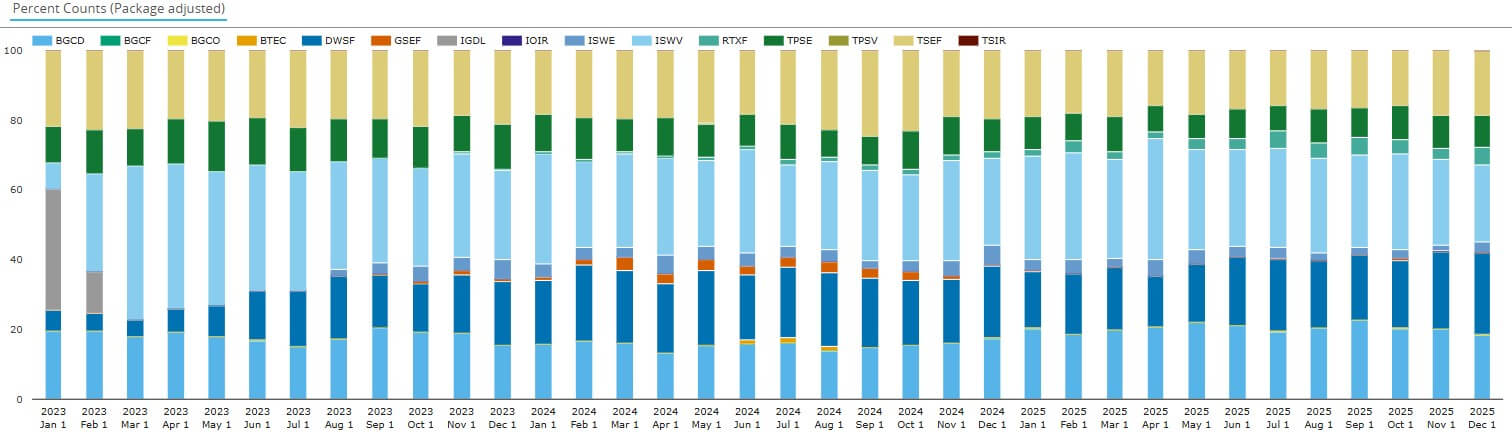

RTX market share

Chart 3: SDR-reported share of cleared SOFR swaps risk-trading volume by D2D platform (execution event count excluding compression). Source: SDRView

Chart 3 shows the emergence of RTX (in pale green) from its first trade in September 2023 up to the end of 2025. We can summarize the volumes by platform group and compare the December shares each year.

Table 1: SOFR swap risk-trading volume shares by D2D platform group (percentage of execution events). Source: SDRView

Table 1 is clear enough as it stands. I would highlight that market share moved the most between December 2023 and December 2025 from the voice-brokerage-based TP ICAP (down 9.0 percent) to the session-based Dealerweb (up 5.4 percent), and the RFT-based RTX (up 4.9 percent).

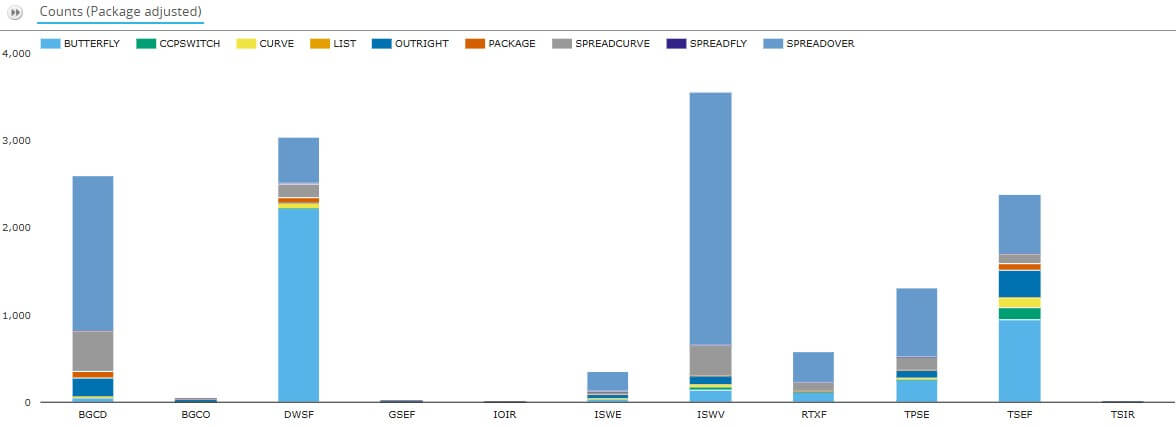

We can also show the package type composition of each platform’s volumes.

Chart 4: 2025 SDR-reported D2D platform SOFR swaps risk-trading volume by package type and platform (execution event count excluding compression). Source: SDRView

Chart 4 shows a package type breakdown of volumes for each platform ID.

- TP ICAP’s volumes (from IOIR, ISWE, ISWV, TPSE, TSIR) are led by spreadovers, then curve spreads (SPREADCURVE), then butterflies, then outrights.

- Dealerweb’s volumes are led by butterflies, then spreadovers, then curve spreads, then curve trades.

- BGC’s volumes (from BGCD, BGCO, GSEF) are led by spreadovers, then curve spreads and outrights.

- Tradition’s (TSEF’s) volumes are led by butterflies, then spreadovers, then outrights, then curve trades, then CCP switches.

- RTX’s volumes are led by spreadovers, then butterflies, then curve spreads, establishing itself in each of the three leading package types from chart 2.

Overall, RTX has reached a 5.1 percent share of December 2025 volumes of D2D SOFR swap risk trading execution event count – two and a quarter years from their first trade.

What are RTX’s expansion possibilities?

While RTX’s five percent share in December is meaningful, RTX noted further growth possibilities in SOFR swaps:

- In addition to the 18 banks already on the platform (per the RTX website), another 12 major US-based swap dealers are in the pipeline.

- RTX can be adopted by business lines beyond the USD swap desk in each participant (for example: US-based bond issuance, syndication, treasury, cross-currency swaps, and FX trading).

- RTX plans to open in Europe in 2025, allowing the platform to open 5 or 6 hours earlier, targeting the material SOFR swaps activity in the European morning.

- Banks can be brought on that don’t have a US-based SOFR swap desk, beyond the 30 noted above.

RTX website certifications show RTX’s intent to expand beyond SOFR to USD basis swaps and swaps based on EUR Euribor, EUR ESTR, GBP SONIA, and JPY TONA.

That’s it

Skip back to the top to reread the key takeaways if you like.

You can find a lot more data in CCPView, SDRView, SEFView, and SBSDRView. Click each link to see a summary of the range of data available.

Contact us if you are interested in a subscription.

Stay informed with our FREE newsletter, subscribe here.

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.