Asia family offices: Appetite for PE increases, but regional GPs are left wanting

This content was originally published by ION Analytics.

Key Takeaways

- As family offices multiply, PE investment increases, but numbers are deceptive.

- Most families mimic global institutional strategies favouring Western markets.

- Asian GPs will leverage the wave where families pursue contrarian strategies.

The first rule of analysing the behaviour of family offices is to acknowledge that all family offices are unique. So, when they appear to be moving en masse, two questions must be asked. First, is there really a common motivator for the trend? Second, how many of them are bona fide family offices?

For private equity investors in Asia hoping to tap this source of capital, such caution bears keeping in mind amidst a seeming groundswell of family office creation in the region. Much of the expectation is centred on Singapore, where the number of family offices registered with the Monetary Authority of Singapore has ballooned from 400 in 2020 to 1,650 as of mid-September.

The growth spurt overlaps a macro slowdown that has pinched fundraising, a global investor exodus from China with some contagion effect across Asia, and an industrywide shift toward the participation of private wealth in the asset class. Yet the diverse nature of the family office space makes it difficult to connect the dots.

“There’s this perception that new family offices are opening so quickly, but the number of family offices in Singapore with a senior private equity professional like me is still extremely low,” said Sam Robinson, managing partner at North East Private Equity Asia, the regional arm of a family office established by the founders of jewellery retailer Pandora.

“The reasons for them setting up here are so varied. It might just be moving some assets offshore from the US or to set up an administrative department. If they’re investing, sometimes it’s just one person doing everything.”

Still, the rise of family offices as a source of capital for Asian private equity can be discerned by the proliferation of various intermediaries and tools, including multi-family offices (MFOs), external asset managers (EAMs), boutique advisories, enhanced liquidity products, specialised online platforms, and fund-of-funds.

“Conservatively, in the past year, a good 40-50 new entities have popped up in every different format, level of quality yet to be confirmed,” said Vincent Ng, a Hong Kong-based partner at placement agent Atlantic Pacific Capital, though he echoed Robinson’s concern that it can be hard to distinguish genuine pools of capital from phantom structures.

“So anecdotally, we’ve probably more than doubled the private equity coming from the family office side. It depends on the product, but 15%-25% of private equity raised can come from families now.”

Back to school?

The feedback speaks to demand at the more experienced end of the spectrum. Family offices targeted by placement agents to make direct commitments to private equity funds are generally significantly professionalised and already diversified in alternatives. This access point facilitates entry into specific areas of interest such as sector funds and helps maximise co-investment options.

Potentum Partners, an Australia-based private equity-focused advisory that functions like an MFO, helps illustrate the depth of the appetite in terms of family office type.

The firm has more than doubled its number of family office clients to around 320 in the past two years. This spans families with operating businesses and no experience in asset management to well-resourced outfits seeking access to specific strategies.

Potentum is currently building out its team of family office engagement professionals on the expectation of further increases in demand in the near term. To date, 90% of its clients are Australian – partially an outcome of pandemic border closures – but there are plans to tap more Asia-based wealth.

“The family office community is definitely expanding and within that, interest in private markets is expanding, but many don’t know where to start,” said Steve Byrom, who founded Potentum after 11 years as head of private equity at Future Fund, Australia’s sovereign wealth fund.

“They see what they get through their banking relationships and think, ‘There must be more than this. Surely this isn’t how institutions are doing private markets.’ And so we show them what else is out there – it’s more an education process than a sales process.”

Characterising the rising tide of family offices as an education process is a helpful way of defusing expectations that a mountain of private wealth – Blackstone pegs it at USD 80trn globally – is set to flood into the asset class.

Indeed, the influx of family wealth in recent years has done little to offset a broader retraction of institutional capital. The annual average for private equity and venture fundraising targeting Asia for 2020-2023 is USD 191.7bn, according to AVCJ Research, down 13% from the prior four-year period.

The gradual nature of the family wealth phenomenon can be further understood as a function of a generational shift. Family offices led by second or third-generation family members remain a relative rarity in Asia, but they are fast emerging, less tied to the original family business, and seen as more proactive investors.

The trend is partly simple succession, partly economic. Many Asian family-run businesses in traditional, pandemic-weakened industries are under pressure to expedite a purposeful transition. The younger generation’s perceived edge is that they better understand new technologies and business models.

Venture has therefore emerged as a logical first foray of many families in this position. As such, even the largest regional VC managers – which have otherwise graduated to more institutional backing – have benefited from the rise of family interest in innovation.

Jungle Ventures, for example, closed is latest flagship fund on USD 600m in 2022, exceeding a target of USD 350m on the back of surging family office participation. Amit Anand, the firm’s founding partner, told AVCJ at the time that much of this came from Asia and that family offices now represent half the LP base.

“From a mindset perspective, family offices were initially harder to get, but I certainly think that our fortunes are tied in that we’re all operating in these regions,” Anand said. “They can see the disruption or the enablement that the start-up ecosystem is doing better than the global financial institutions.”

Enhanced engagement

While first-generation families have tended to access private markets on an ad hoc basis, intermittently participating in direct deals via their own networks, or in a more structured fashion through private banks, second and third generations have increasingly embraced other channels. This is sometimes part of a learning process of experimenting with independent investment.

“The generational shift in wealth is helpful to us because our value proposition resonates more with the younger generations,” said Jonathan Shelley, COO of Hong Kong-based asset manager 3 Capital Partners, emphasising that a large proportion of his family office clients remain first-generation organisations.

“Initially the second and third generations might want to do it themselves but after a year or two of research, there’s a higher chance they’ll want to work with us rather than try to reinvent the wheel.”

Family offices partnering with the likes of 3 Capital – largely domiciled Greater China and Singapore – are predominantly guided by their principals and networks, rather than professional investment teams. They are overweight Asia, perhaps especially overweight China, seeking diversification out of the region yet wary of US and European managers increasingly shopping funds around Asia.

“The right mindset is to map out the industry and proactively go after the ones you want to invest with,” said Jiahao He, 3 Capital’s CIO. “If you only depend on inbound, you have to ask, why are they coming to me. You always need to be mindful of adverse selection.”

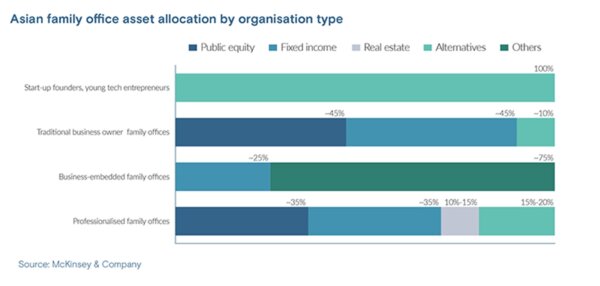

In the background, uptake of private markets has also been underpinned by a longstanding underexposure. First-generation business-owner family offices in Asia that lack professional financial management represent about 20% of regional family wealth and allocate less than 10% to alternatives, not including real estate, according to McKinsey & Company.

These are the groups mostly tapping into MFOs and EAMs to access developed Western markets, propelled by a mix of general diversification needs, frustration with a lack of returns in Asia, and geopolitical anxiety.

The greater opportunity for GPs in risk-off Asian geographies is arguably in regional family offices with professional investment teams. McKinsey finds they represent up to 45% of total family wealth in Asia and have still modest alternatives exposure of 10%-15%, excluding real estate.

“I’m very focused on geopolitics, so we’ll be more sceptical of cross-border strategies that rely on goodwill between certain countries. But we don’t see any geopolitical risk issue with China, so we don’t have to divest,” said one Southeast Asia-based family office CIO, adding that he has backed a China-focused fund as recently as last year.

“Mid to long-term, China is a very strong economy. It’s going through an economic transition, but I’m more bullish than others.”

Horses for courses

Family offices that deal directly with GPs, network proactively at conferences, and minimise reliance on intermediaries generally tend to profile as those more likely to maintain their Asia exposure, according to industry participants.

Their private markets strategy is shifting around the edges, however, with a greater wariness for early-stage venture and more appetite for middle-market buyouts or other strategies perceived as suitable for a higher interest rate environment.

Country-focused family offices, meanwhile, will stick with what they know. In the case of India, a rare developing market with an encouraging stream of private equity exits of late, the asset class is still on the menu despite a recent increase in the capital gains tax rate.

“Traditional business houses are becoming more interested in the start-up space, with more family offices investing in funds or launching their own start-up programs. Many new funds are raising from domestic investors, who are likely to be a bridge for traditional promoters to work with new age start-ups,” said Sheeba D’Mello, head of private capital at Pratithi Investments.

“Exits have been a concern in the industry as there are very few acquisitions. Most start-ups are building for IPOs. There is a resurgence of interest in stable, capital efficient business models. This is another area where collaborations with traditional business houses and family offices can be beneficial for new founders.”

Pratithi, the family office of Infosys co-founder Kris Gopalakrishnan, has seen its exposure to private markets tick up in recent years; it is now about 60% of the overall portfolio. This has coincided with a spike in inbound deal and fund-level opportunities, which have stretched decision-making timeframes.

Multi-jurisdictional family offices can have a less forgiving view on the flood of GP attention that comes with a difficult fundraising environment. One Hong Kong-based family office CIO said that due diligence processes that once took five weeks now take two months due to the need for additional reference calls, site visits, and research reports from third parties.

“We’ve missed out on opportunities because we can’t get comfortable in time, and the filtering process to get to the diligence stage is much narrower,” the CIO said. “But because the performance hasn’t been great, you don’t feel like you’re missing out on much.”

This family office is a professional setup that engages directly with GPs. For those continuing to access private equity via banking relationships, prolonged diligence and missed opportunities could be greater frustrations still.

Roger Suter, who advised family office clients at UBS in Singapore for 11 years before joining Indonesia-focused Northstar Group in 2022 as head of investor relations, observes that his new employer is much more efficient at facilitating co-investment opportunities.

“For a platform like a major bank, providing this kind of offering is much more complex. Significant compliance and legal alignment is required before co-investment opportunities may be offered,” he said. “Family offices can move quickly when interested, but at larger banks, just onboarding a fund for a GP can be a lengthy process due to the extensive approvals and procedures involved.”

Northstar, a largely middle market focused GP, engaged Suter to bring family offices into its debut VC fund, which closed on USD 140m in 2022. Still, most of the corpus came from institutional LPs.

Northstar’s minimum cheque size requirements and relatively niche strategy made it difficult to accommodate most family offices in the region. Those accessing GPs via MFOs and EAMs had their sights primarily on the US. That left Suter to engage directly with a limited universe of well-resourced family offices that still have appetite for Southeast Asia venture.

Big picture concerns

Meanwhile, geopolitical uncertainty continues to rumble, perhaps most noisily in family office ears. According to a recent survey by UBS, 58% of family offices globally see a major geopolitical conflict as their biggest risk in the coming 12 months. This far outstrips the next biggest concerns, higher inflation and real estate correction, which each scored 39%.

“We assess companies for single-asset investments through their geopolitical exposure. Even if we only put USD 5m-USD 10m into it, we will read all the latest US Congress papers to see what kind of risks there could be,” said Nick Xiao, founder and CEO of Annum Capital, a Hong Kong-based MFO.

“The way our clients look at geographies and sectors has changed a lot – previously Greater China-oriented, now very global. They are keen to learn about Southeast Asia, US onshore, and continental Europe. If a family office had USD 100m for private equity 18 months ago, it’s now USD 120m, but more than USD 80m of that has moved.”

The main motivators for these relocations remain the quest for diversification and an unwillingness to re-up in Asia amidst stalled returns. But the fact that so many family offices flag geopolitical risk as a primary consideration speaks volumes about their tendency to think of portfolio construction in terms beyond the systematic maximisation of returns.

In this way, the most promising beacon of hope for Asian GPs seeking to access newly mobilised family offices goes back to their diversity. There is a wildcat flavour to family offices in that they often have unique strategic interests and personality-driven decision making.

Direct investments are a convenient window into this culture. Investment in dubious trophy assets has been a feature of Asian family office activity since the global financial crisis. “These are very sophisticated setups with more than USD 500m in assets. They tried to do private directs and most of them have failed,” said one MFO executive.

For family offices that have spent time as LPs, direct activity has broadly shifted toward co-investment, but these openings still come with a two to six-week window to react. Even large, professionalised family offices may not be able to properly process these opportunities independently. The result is sometimes a gut decision.

“Family offices all dream about doing direct private equity, but at the end of the day, the best talent will go with organisations that have decades of success where they’re paid a huge amount of carry,” said Anthony Chan, CEO of Hong Kong-based MFO Isola Capital.

“You can be some of the richest people in the world, but you won’t attract that kind of talent to form a team at your family office. That’s something families don’t always consider.”

Most of Isola’s clients emulate the strategies of global sovereign wealth funds and endowments by making North America 75%-80% of their portfolios. While committee-advised approaches will continue to pivot in this direction, families with top-down power structures and contrarian strategies may also increasingly turn to developing markets.

Asian epiphany?

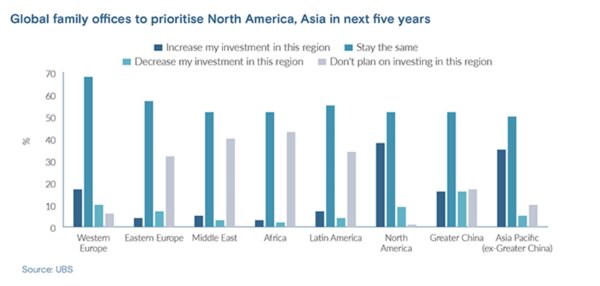

There is some evidence to suggest that Asia will benefit from this effect more than other developing markets. In UBS’s survey of global family offices, 35% of respondents said they would increase their investment in Asia Pacific ex-China in the next five years. This was second only to North America on 38% and well ahead of Greater China (16%), Latin America (7%) and Africa (3%).

“There’s a compelling story for Asia on many levels. It’s still a growth market overall and for the right managers that can differentiate themselves, there’s an opportunity there. Those managers should take some solace that all boats should rise with the tide of family offices,” said Ben Hart, head of investor relations for Asia ex-Japan at Adams Street Partners.

“When I do hear comments about China being oversold, it tends to be from the principal rather than a team that has been hired to be more thoughtful about portfolio construction and building out broader diversification with global exposures. Where the principal is directly involved is where you’re more likely to see that kind of risk-taking appetite.”

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.