Navigating a new era of risk management: why energy firms must adapt at pace

[This content was originally published by TabbFORUM.]

In recent years, commodity trading firms have thrived despite significant macroeconomic turbulence.[1] However, the market bucked this upward trend in 2023, observing a fractional decline in key indexes due to cooling inflation.[2] Continuing volatility in 2024 confirms that the risk environment is not likely to settle anytime soon.

Against escalating geopolitical tensions and persistent economic uncertainty, commodities traders and investors need a clear view of risk to make sound strategic decisions. With high volatility and unpredictable disruptions, it is in the best interest of all stakeholders to put risk management at the top of their agenda to understand how adverse market events may impact profitability.

This increasing emphasis on risk has led to step-changing innovation in recent years.

The old days of risk management

While countless risk management methodologies are now available, none rival the enduring popularity of Value-at-Risk (VaR), which quantifies a portfolio’s potential loss over a specified time horizon, at a given confidence level. VaR provides a single numerical estimate of the potential downside risk, helping financial institutions, traders, and investors gauge and manage their exposure to market fluctuations and unforeseen events.

The adoption of VaR surged following J.P. Morgan’s 1995 publication of the detailed calculation methodology for their RiskMetrics model. The following year, the Bank for International Settlements’ (BIS) endorsement of the model for determining market risk capital requirements bolstered VaR’s use.

VaR calculations initially relied on a parametric approach, which used statistical formulas assuming returns following a normal distribution to evaluate risk. The later introduction of the Monte Carlo VaR methodology improved risk assessment accuracy by simulating a wide range of possible future outcomes. This development enabled a fuller evaluation of options and other nonlinear products across various scenarios instead of estimating the P&L changes from the linear (delta) assumption of parametric VaR.

Another evolution of the risk methodology is historical VaR. While parametric and Monte Carlo VaR assume normal distributions of price returns, historical VaR uses actual historical returns to provide a more realistic risk assessment. This approach is particularly relevant in commodity markets, where extreme price changes are observed more often than the normal distribution suggests. Using real-world events to represent the universe of scenarios, this methodology addresses the scope for inaccuracies of theoretical models based solely on statistical assumptions.

Risk management using VaR today

In an environment of heightened complexity and volatility, traders now face increasing challenges to evaluate and manage risk accurately with VaR.

Though VaR remains widely adopted, risk management reporting practices are constantly evolving. Given the fast past of commodity markets, traders cannot afford to wait hours for new results. Traders desire real-time VaR estimates when adding new trade positions to their portfolios. Thanks to rapid improvements in computing speed, intense VaR processing is now affordable, allowing further applications beyond one-and-done VaR analytics.

Furthermore, Risk Managers are increasingly tasked with explaining VaR fluctuations at a more granular level from day-to-day. The requirement is complicated by the many moving factors that influence their exposures, including price, position, volatility, and correlation. Comprehensively answering these questions often requires repeated VaR computations.

Changing commodity price behavior is another complexity for risk managers in the energy markets. For instance, the proliferation of renewable generation has brought new power price behavior to light; as solar production peaks during the day, a power surplus can cause the power price to become negative. Thus, realistic risk models must accommodate the possibility of occasional negative prices. Monte Carlo simulations are ideal for creating scenarios with negative prices.

Cash Flow at Risk (CFaR) and Potential Future Exposure (PFE)

VaR is not the appropriate risk management tool for investors managing assets with long-term cash flows, like natural gas storage or renewable generation assets due to its focus on short-time horizons. So, a different approach is often used: Cash Flow at Risk (CFaR). Similar to Monte Carlo VaR, CFaR calculates the cumulative, realized portfolio cash flows generated from multi-step price and production simulations but at various horizons.

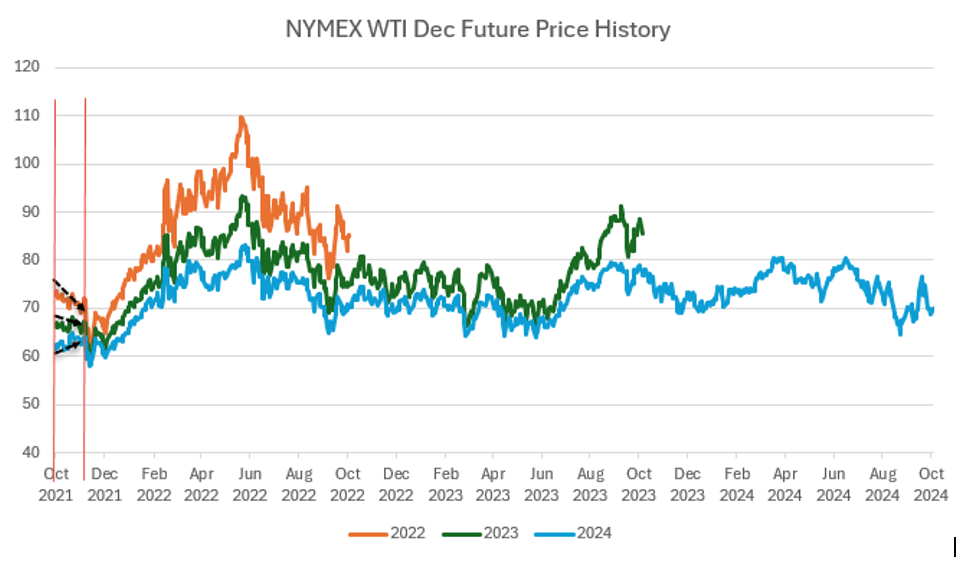

The diagrams below contrast how risk is measured between VaR and CFaR. Three different NYMEX WTI December futures expire in 2022, 2023 and 2024. In Figure 1, the black arrows represent the short-term risk measured by VaR from the reporting date to the holding period across all assets.

Figure 1: Period of short-term risk from the reporting date to the holding period measured by VaR

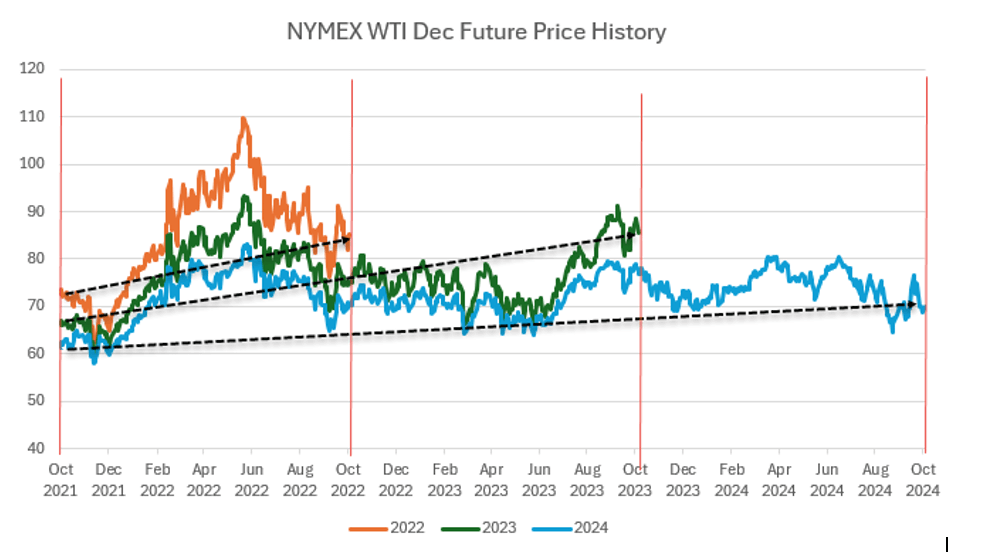

In Figure 2, the black arrows represent the risk specific to the asset maturity that CFaR measures.

Figure 2: Maturity-specific risk from the reporting date to the asset expiration date measured by CFaR

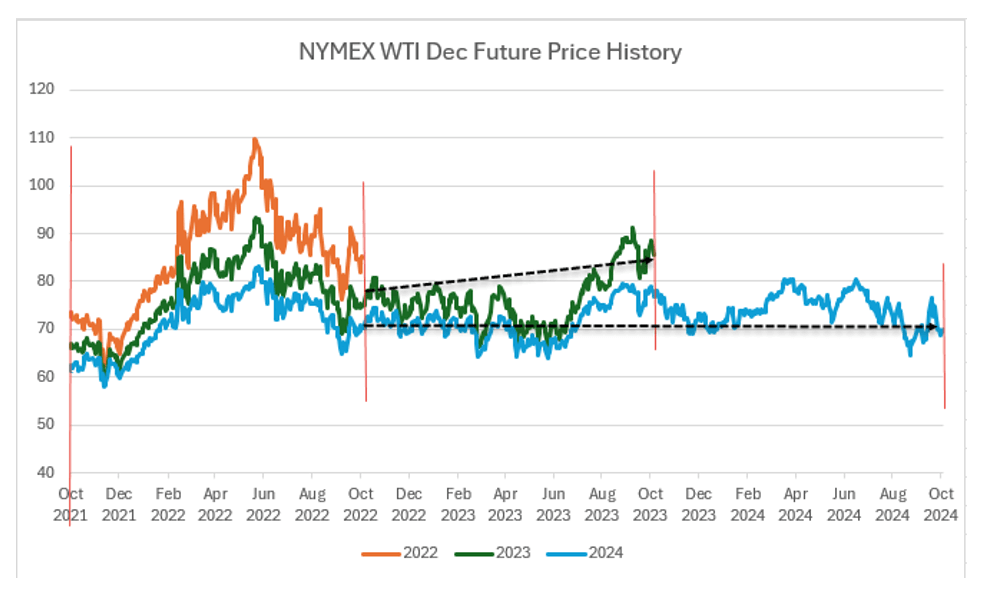

Another – Monte Carlo risk methodology adaptation is Potential Future Exposure (PFE). PFE measures the counterparty market risk at a given confidence level, should the counterparty default on potentially profitable open trade obligations, now or in the future. The risk is observed at various time horizons, creating snapshots of how the risk will peak and change over time. Credit Analysts can use the information to advise on the counterparty collateral management plan accordingly.

In Figure 3, consider the same previous portfolio at the observed time horizon in Oct 2022. Only unexpired futures for 2023 and 2024 are considered risky for credit risk exposure in calculating PFE.

Figure 3: Period of risk measured by PFE for the Oct 2022 time horizon.

Reliable and versatile analytics

Amidst significant volatility across the commodities market, traders increasingly require reliability and versatility in their risk management tools to gain a competitive edge. It is important to understand the unique characteristics of each portfolio thoroughly and have a tailored plan to manage the risk. Risk management can improve with committed investment in the right tools and people. Well-designed risk analytics that support a range of analytical needs are required to measure risk effectively. These include parametric, Monte Carlo Simulation, Historical Simulation VaR, CFaR, and PFE, with varying emerging assumptions and applications.

Risk managers must be able to forecast VaR changes promptly in the event of new trades and provide various supporting data to help explain the calculation. Software-as-a-service (SaaS) risk analytics solutions, readily integrated with data from a commodity management system, can promptly support the increased computational demand stemming from business growth or the iterative computations necessary for better understanding risk exposure. Ultimately, these tools can help risk managers automate their risk reporting, freeing time and energy for better client service.

[1] https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/the-future-of-commodity-trading

[2] https://www.bloomberg.com/professional/blog/indices-2024-outlook-global-commodities/

Don't miss out

Subscribe to our blog to stay up to date on industry trends and technology innovations.